Week 4: Overfitting / MCMC

The fourth week covers Chapter 7 (Ulysses’ Compass), Chapter 8 (Conditional Manatees), and Chapter 9 (Markov Chain Monte Carlo).

4.2 Exercises

4.2.1 Chapter 7

7E1. State the three motivating criteria that define information entropy. Try to express each in your own words.

Information is defined as the reduction in uncertainty when we learn and outcome. The motivating criteria for defining information entropy revolve around the measure of uncertainty that is used to derive information.

The first is that the measure of uncertainty must be continuous. This prevents large changes in the uncertainty measure resulting from relatively small changes in probabilities. Such a phenomenon often occurs when researchers use a p-value cutoff of .05 to claim “significance.” Often, the difference between “significant” and “non-significant” results is itself non-significant 🤯.

The second is that the measure of uncertainty should increase as the number of possible events increases. When there are more potential outcomes, there are more predictions that have to be made, and therefore more uncertainty about which outcome will be observed. For example, if your friend asks you to guess a number between 1 and 100, you are much less likely to guess correctly than if you were guessing a number between 1 and 2.

The third and final criteria is that the measure of uncertainty should be additive. These means that if we calculate the uncertainty for two sets of outcomes (e.g., heads or tail on a coin flip and the results of a thrown die), then the uncertainty of combinations of events (e.g., heads and “3”) should be equal to the sum of the uncertainties from the two separate events.

Information entropy is the only function that satisfies all three criteria.

7E2. Suppose a coin is weighted such that, when it is tossed and lands on a table, it comes up heads 70% of the time. What is the entropy of this coin?

Entropy is the average log-probability of an event. The formula is given as

\[\begin{equation} H(p) = -\text{E}\log(p_i) = -\sum_{i=1}^np_i\log(p_i) \end{equation}\]

Thus, for each probability \(p_i\), we multiply \(p_i\) by \(\log(p_i)\), sum all the values, and then multiply the sum by negative one. To implement this, we’ll first write a couple of functions to do the calculations. We could do this without functions, but functions will allow us to handle cases where \(p_i = 0\), as will be the case in a couple of problems. The first function, p_logp(), returns 0 if p is 0, and returns p * log(p) otherwise. The calc_entropy() function is a wrapper around p_logp(), applying p_logp() to each element of a vector of probabilities, summing the results, and multiplying the sum by -1.

p_logp <- function(p) {

if (p == 0) return(0)

p * log(p)

}

calc_entropy <- function(x) {

avg_logprob <- sum(map_dbl(x, p_logp))

-1 * avg_logprob

}Applying these functions to the probabilities in this problem results in an entropy of about 0.61. Note this is the same as the weather example in the text, because in both cases there were two events with probabilities of 0.3 and 0.7.

probs <- c(0.7, 0.3)

calc_entropy(probs)

#> [1] 0.6117E3. Suppose a four-sided die is loaded such that, when tossed onto a table, it shows “1” 20%, “2” 25%, “3” 25%, and “4” 30% of the time. What is the entropy of this die?

Now we have four outcomes. We can reuse our code from above, substituting the new probabilities into the vector probs. This results in an entropy of about 1.38. As expected, because there are now more outcomes, the entropy is higher than what was observed in the previous problem.

probs <- c(0.20, 0.25, 0.25, 0.30)

calc_entropy(probs)

#> [1] 1.387E4. Suppose another four-sided die is loaded such that it never shows “4.” The other three sides show equally often. What is the entropy of this die?

Again, we can copy our code from above, replace the probabilities. Even though there are four outcomes specified, there are effectively three outcomes, as the outcome “4” has probability 0. Thus, we would expect entropy to decrease, as there are fewer possible outcomes than in the previous problem. This is indeed what we find, as this die’s entropy is about 1.1.

probs <- c(1, 1, 1, 0)

probs <- probs / sum(probs)

probs

#> [1] 0.333 0.333 0.333 0.000

calc_entropy(probs)

#> [1] 1.17M1. Write down and compare the definitions of AIC and WAIC. Which of these criteria is most general? Which assumptions are required to transform the more general criterion into a less general one?

The AIC is defined as follows, where \(\text{lppd}\) is the log-pointwise-predictive density, and \(p\) is the number of free parameters in the posterior distribution.

\[ \text{AIC} = -2\text{lppd} + 2p \]

In contrast, the WAIC is defined as:

\[ \text{WAIC}(y,\Theta) = -2\Big(\text{lppd} - \sum_i \text{var}_{\theta}\log p(y_i | \theta)\Big) \]

If we distribute the \(-2\) through, this looks remarkably similar to the AIC formula, with the exception of the final \(p\) term. Whereas the AIC uses 2 times the number of free parameters, the WAIC uses 2 times the sum of the log-probability variances from each observation.

The WAIC is more general than the AIC, as the AIC assumes that priors are flat or overwhelmed by the likelihood, the posterior distribution is approximately multivariate Gaussian, and the sample size is much greater than the number of parameters. If all of these assumptions are met, then we would expect the AIC and WAIC to be about the same.

7M2. Explain the difference between model selection and model comparison. What information is lost under model selection?

Model selection refers to just picking the model that has the lowest (i.e., best) criterion value and discarding other models. When we take this approach, we lose information about the relative model accuracy that can be seen across the criterion values for the candidate models. This information can inform how confident we are in the models. Additionally, the model selection paradigm cares only about predictive accuracy and ignores causal inference. Thus, a model may be selected that has confounds or that would not correctly inform an intervention.

In contrast, model comparison uses multiple models to understand how the variables included influence prediction and affect implied conditional independencies in a causal model. Thus, we preserve information and can make more holistic judgments about our data and models.

7M3. When comparing models with an information criterion, why must all models be fit to exactly the same observations? What would happen to the information criterion values, if the models were fit to different numbers of observations? Perform some experiments, if you are not sure.

All of the information criteria are defined based on the log-pointwise-predictive density, defined as follows, where \(y\) is the data, \(\Theta\) is the posterior distribution, \(S\) is the number of samples, and \(I\) is the number of samples.

\[ \text{lppd}(y,\Theta) = \sum_i\log\frac{1}{S}\sum_sp(y_i|\Theta_s) \]

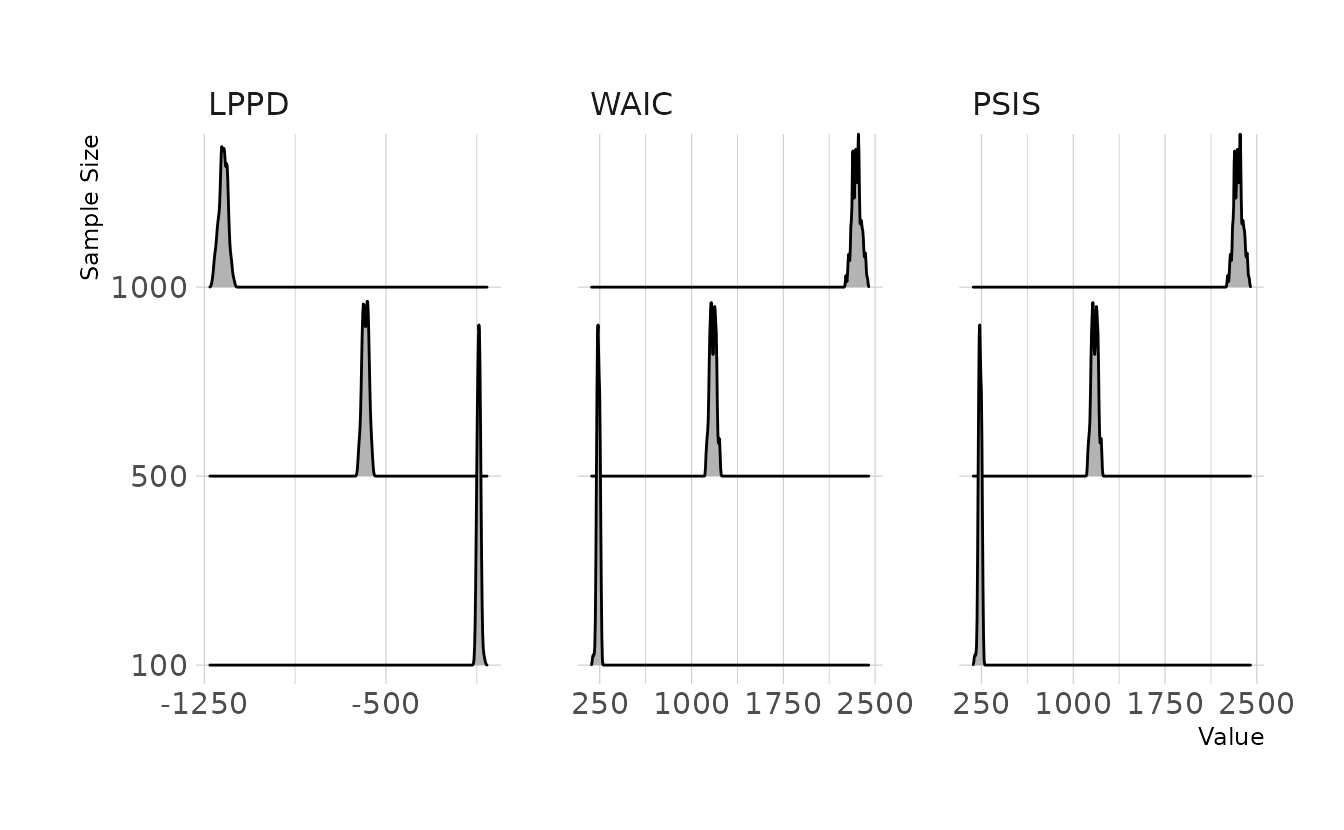

In words, this means take the log of the average probability across samples of each observation \(i\) and sum them together. Thus, a larger sample size will necessarily lead to a smaller log-pointwise-predictive-density, even if the data generating process and models are exactly equivalent (i.e., when the LPPD values are negative, the sum will get more negative as the sample size increases). More observations are entered into the sum, leading to a smaller final lppd, which will in turn increase the information criteria. We can run a quick simulation to demonstrate. For three different sample sizes, we’ll simulate 100 data sets from the exact same data generation process, estimate a the exact same linear model, and then calculate the LPPD, WAIC, and PSIS for each.

Visualizing the distribution of the LPPD, WAIC, and PSIS across simulated data sets with each sample size, we see that the LPPD gets more negative as the sample size increases, even though the data generation process and estimated model are identical. Accordingly, the WAIC and PSIS increase. Note that the WAIC and PSIS values are approximately \(-2 \times \text{lppd}\). Thus, if we fit one model with 100 observations and second model with 1,000 observations, we might conclude from the WAIC and PSIS that the first model with 100 observations has much better predictive accuracy, because the WAIC and PSIS values are lower. However, this would be only an artifact of different sample sizes, and may not actually represent true differences between the models.

Simulation Code

gen_data <- function(n) {

tibble(x1 = rnorm(n = n)) %>%

mutate(y = rnorm(n = n, mean = 0.3 + 0.8 * x1),

across(everything(), standardize))

}

fit_model <- function(dat) {

suppressMessages(output <- capture.output(

mod <- brm(y ~ 1 + x1, data = dat, family = gaussian,

prior = c(prior(normal(0, 0.2), class = Intercept),

prior(normal(0, 0.5), class = "b"),

prior(exponential(1), class = sigma)),

iter = 4000, warmup = 3000, chains = 4, cores = 4, seed = 1234)

))

return(mod)

}

calc_info <- function(model) {

mod_lppd <- log_lik(model) %>%

as_tibble(.name_repair = "minimal") %>%

set_names(paste0("obs_", 1:ncol(.))) %>%

rowid_to_column(var = "iter") %>%

pivot_longer(-iter, names_to = "obs", values_to = "logprob") %>%

mutate(prob = exp(logprob)) %>%

group_by(obs) %>%

summarize(log_prob_score = log(mean(prob))) %>%

pull(log_prob_score) %>%

sum()

mod_waic <- suppressWarnings(waic(model)$estimates["waic", "Estimate"])

mod_psis <- suppressWarnings(loo(model)$estimates["looic", "Estimate"])

tibble(lppd = mod_lppd, waic = mod_waic, psis = mod_psis)

}

sample_sim <- tibble(sample_size = rep(c(100, 500, 1000), each = 100)) %>%

mutate(sample_data = map(sample_size, gen_data),

model = map(sample_data, fit_model),

infc = map(model, calc_info)) %>%

select(-sample_data, -model) %>%

unnest(infc) %>%

write_rds(here("fits", "chp7", "b7m3-sim.rds"), compress = "gz")

library(ggridges)

sample_sim %>%

pivot_longer(cols = c(lppd, waic, psis)) %>%

mutate(sample_size = fct_inorder(as.character(sample_size)),

name = str_to_upper(name),

name = fct_inorder(name)) %>%

ggplot(aes(x = value, y = sample_size)) +

facet_wrap(~name, nrow = 1, scales = "free_x") +

geom_density_ridges(bandwidth = 4) +

scale_y_discrete(expand = c(0, .1)) +

scale_x_continuous(breaks = seq(-2000, 3000, by = 750)) +

coord_cartesian(clip = "off") +

labs(x = "Value", y = "Sample Size")

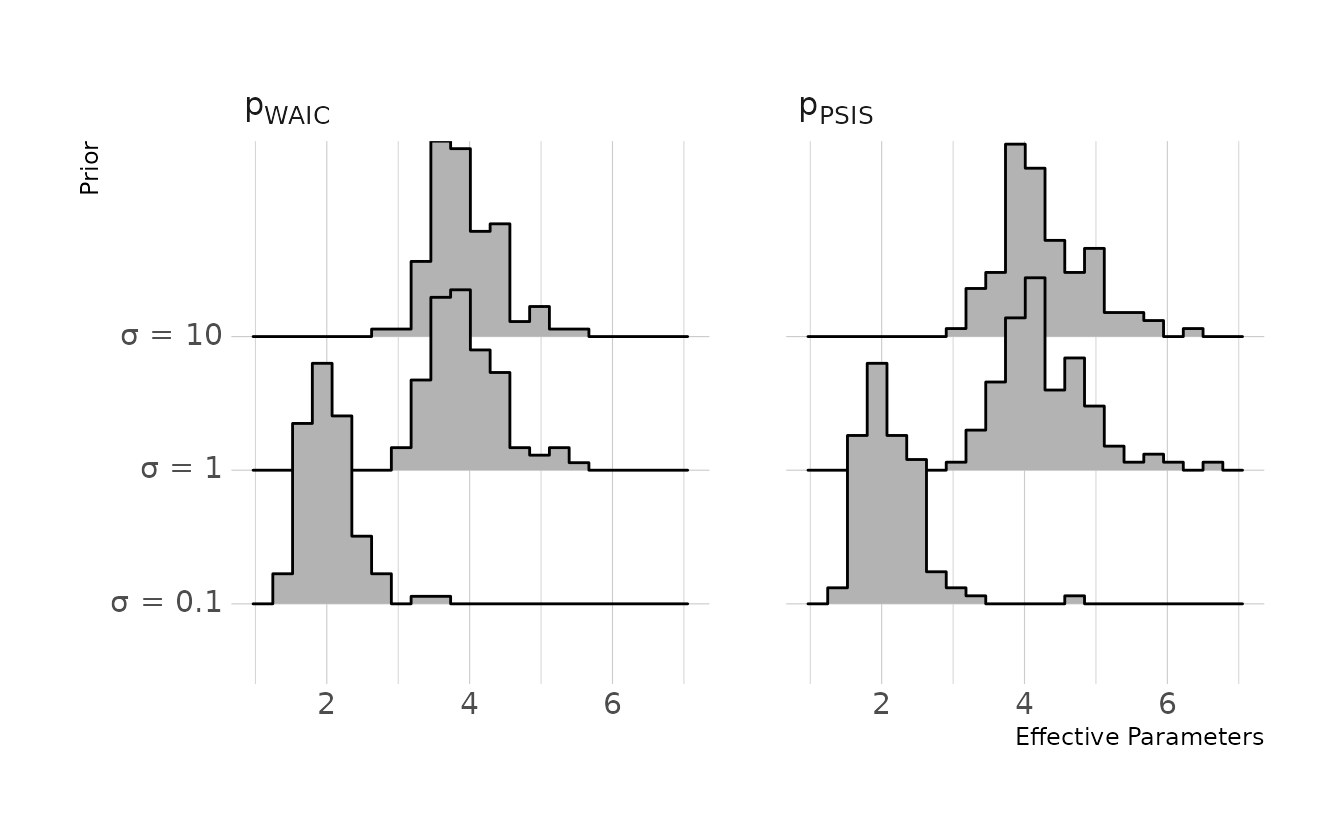

7M4. What happens to the effective number of parameters, as measured by PSIS or WAIC, as a prior becomes more concentrated? Why? Perform some experiments, if you are not sure.

The penalty term of the WAIC, \(p_{\Tiny\text{WAIC}}\) is defined as shown in the WAIC formula. Specifically, the penalty term is sum of the variances of the log probabilities for each observation.

\[ \text{WAIC}(y,\Theta) = -2\Big(\text{lppd} - \underbrace{\sum_i \text{var}_{\theta}\log p(y_i | \theta)}_{\text{penalty term}}\Big) \]

Smaller variances in log probabilities will results in a lower penalty. If we restrict the prior to become more concentrated, we restrict the plausible range of the parameters. In other words, we restrict the variability in the posterior distribution. As the parameters become more consistent, the log probability of each observation will necessarily become more consistent also. Thus, the penalty term, or effective number of parameters, becomes smaller. We can again confirm with a small simulation.

In this simulation we keep everything constant (i.e., data generation, model), with the exception of the prior for the slope coefficients. We’ll try three different priors: \(\text{Normal}(0, 0.1)\), \(\text{Normal}(0, 1)\), and \(\text{Normal}(0, 10)\). Visualizing the results, we can see that the more constricted prior does indeed result in a smaller penalty or effective number of parameters.

Simulation Code

gen_data <- function(n) {

tibble(x1 = rnorm(n = n),

x2 = rnorm(n = n),

x3 = rnorm(n = n)) %>%

mutate(y = rnorm(n = n, mean = 0.3 + 0.8 * x1 +

0.6 * x2 + 1.2 * x3),

across(everything(), standardize))

}

fit_model <- function(dat, p_sd) {

suppressMessages(output <- capture.output(

mod <- brm(y ~ 1 + x1 + x2 + x3, data = dat,

family = gaussian,

prior = c(prior(normal(0, 0.2), class = Intercept),

prior_string(glue("normal(0, {p_sd})"), class = "b"),

prior(exponential(1), class = sigma)),

iter = 4000, warmup = 3000, chains = 4, cores = 4, seed = 1234)

))

return(mod)

}

calc_info <- function(model) {

w <- suppressWarnings(brms::waic(model))

p <- suppressWarnings(brms::loo(model))

tibble(p_waic = w$estimates["p_waic", "Estimate"],

p_loo = p$estimates["p_loo", "Estimate"])

}

prior_sim <- tibble(sample_size = 20,

prior_sd = rep(c(0.1, 1, 10), each = 100)) %>%

mutate(sample_data = map(sample_size, gen_data),

model = map2(sample_data, prior_sd, fit_model),

infc = map(model, calc_info)) %>%

select(-sample_data, -model) %>%

unnest(infc) %>%

write_rds(here("fits", "chp7", "b7m4-sim.rds"), compress = "gz")

prior_sim %>%

pivot_longer(cols = c(p_waic, p_loo)) %>%

mutate(prior_sd = glue("σ = {prior_sd}"),

prior_sd = fct_inorder(prior_sd),

name = factor(name, levels = c("p_waic", "p_loo"),

labels = c("p<sub>WAIC</sub>", "p<sub>PSIS</sub>"))) %>%

ggplot(aes(x = value, y = prior_sd, height = stat(density))) +

facet_wrap(~name, nrow = 1) +

geom_density_ridges(stat = "binline", bins = 20) +

labs(x = "Effective Parameters", y = "Prior") +

theme(axis.text.y = element_markdown())

7M5. Provide an informal explanation of why informative priors reduce overfitting.

Informative priors restrict the plausible values for parameters. By using informative priors, we can limit the values of parameters to values that are reasonable, given our scientific knowledge. Thus, we can keep the model from learning too much from our specific sample.

7M6. Provide an informal explanation of why overly informative priors result in underfitting.

In contrast to the previous question, making the prior too informative can be too restrictive on the parameter space. This prevents our model from learning enough from our sample. We basically just get our prior distributions back, without learning anything from the data that could help make future predictions.

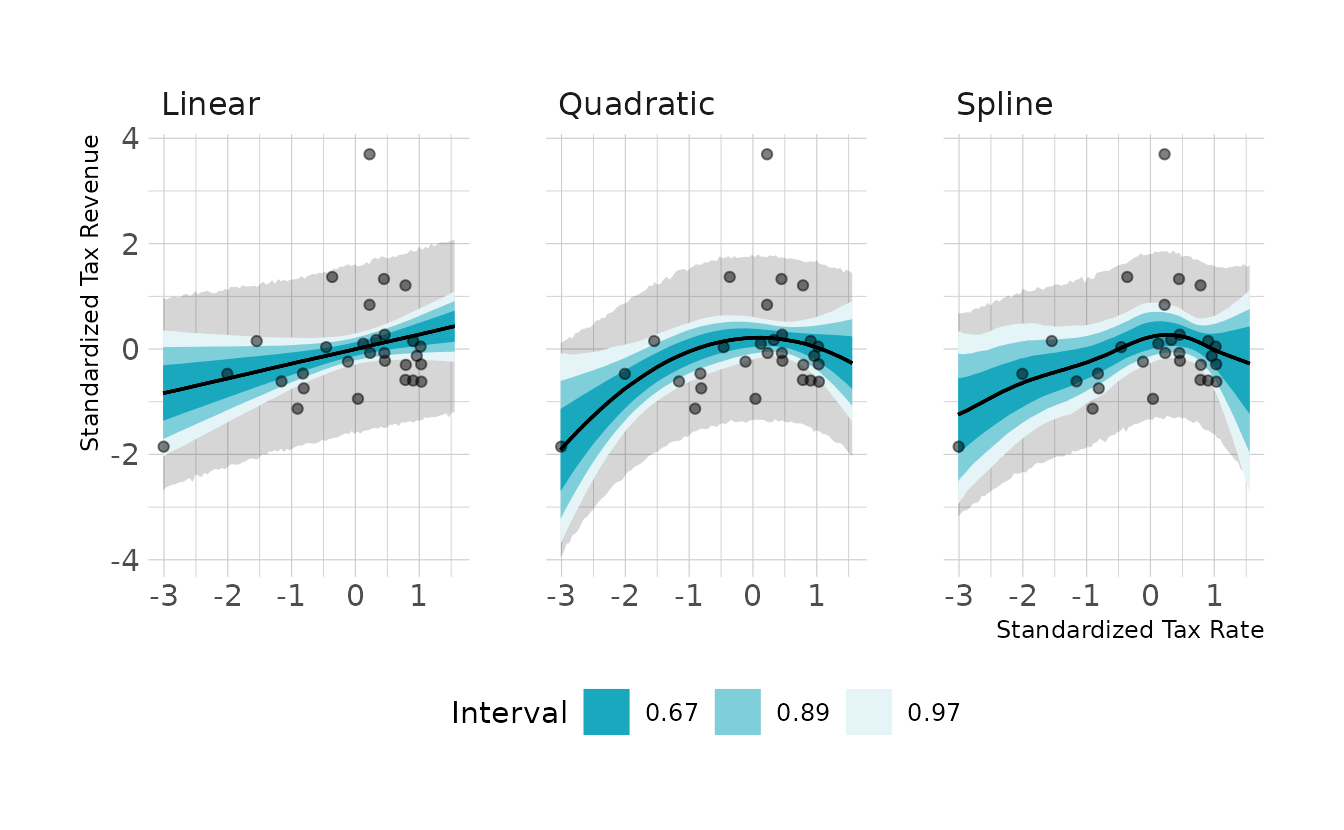

7H1. In 2007, The Wall Street Journal published an editorial (“We’re Number One, Alas”) with a graph of corportate tax rates in 29 countries plotted against tax revenue. A badly fit curve was drawn in (reconstructed at right), seemingly by hand, to make the argument that the relationship between tax rate and tax revenue increases and then declines, such that higher tax rates can actually produce less tax revenue. I want you to actually fit a curve to these data, found in

data(Laffer). Consider models that use tax rate to predict tax revenue. Compare, using WAIC or PSIS, a straight-line model to any curved models you like. What do you conclude about the relationship between tax rate and tax revenue.

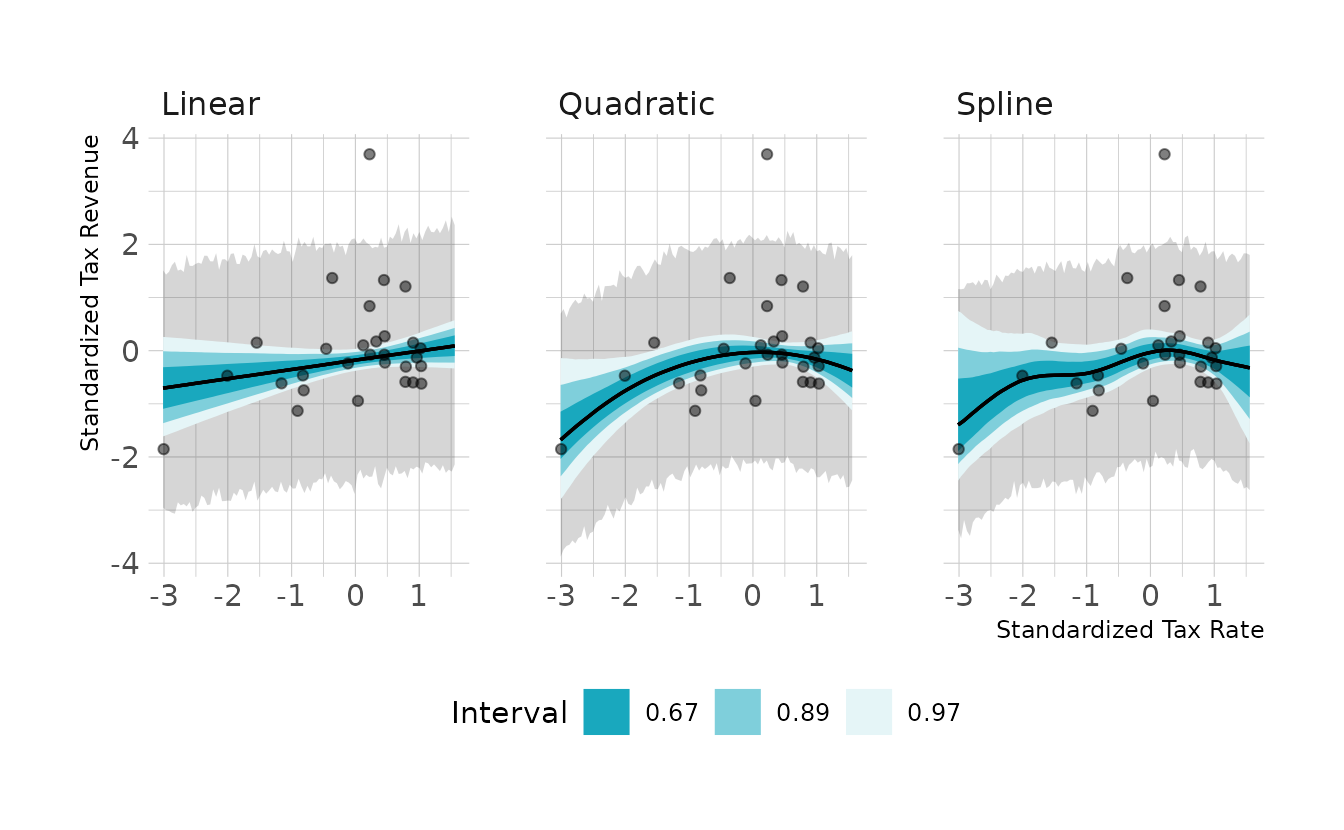

First, let’s standardize the data and fit a straight line, a quadratic line, and a spline model.

data(Laffer)

laf_dat <- Laffer %>%

mutate(across(everything(), standardize),

tax_rate2 = tax_rate ^ 2)

laf_line <- brm(tax_revenue ~ 1 + tax_rate, data = laf_dat, family = gaussian,

prior = c(prior(normal(0, 0.2), class = Intercept),

prior(normal(0, 0.5), class = b),

prior(exponential(1), class = sigma)),

iter = 4000, warmup = 2000, chains = 4, cores = 4, seed = 1234,

file = here("fits", "chp7", "b7h1-line.rds"))

laf_quad <- brm(tax_revenue ~ 1 + tax_rate + tax_rate2, data = laf_dat,

family = gaussian,

prior = c(prior(normal(0, 0.2), class = Intercept),

prior(normal(0, 0.5), class = b),

prior(exponential(1), class = sigma)),

iter = 4000, warmup = 2000, chains = 4, cores = 4, seed = 1234,

file = here("fits", "chp7", "b7h1-quad.rds"))

laf_spln <- brm(tax_revenue ~ 1 + s(tax_rate, bs = "bs"), data = laf_dat,

family = gaussian,

prior = c(prior(normal(0, 0.2), class = Intercept),

prior(normal(0, 0.5), class = b),

prior(normal(0, 0.5), class = sds),

prior(exponential(1), class = sigma)),

iter = 4000, warmup = 2000, chains = 4, cores = 4, seed = 1234,

control = list(adapt_delta = 0.95),

file = here("fits", "chp7", "bh71-spln.rds"))Let’s visualize the models:

Code to reproduce

tr_seq <- tibble(tax_rate = seq(0, 40, length.out = 100)) %>%

mutate(tax_rate = (tax_rate - mean(Laffer$tax_rate)) / sd(Laffer$tax_rate),

tax_rate2 = tax_rate ^ 2)

predictions <- bind_rows(

predicted_draws(laf_line, newdata = tr_seq) %>%

median_qi(.width = 0.89) %>%

mutate(type = "Linear"),

predicted_draws(laf_quad, newdata = tr_seq) %>%

median_qi(.width = 0.89) %>%

mutate(type = "Quadratic"),

predicted_draws(laf_spln, newdata = tr_seq) %>%

median_qi(.width = 0.89) %>%

mutate(type = "Spline")

)

fits <- bind_rows(

epred_draws(laf_line, newdata = tr_seq) %>%

median_qi(.width = c(0.67, 0.89, 0.97)) %>%

mutate(type = "Linear"),

epred_draws(laf_quad, newdata = tr_seq) %>%

median_qi(.width = c(0.67, 0.89, 0.97)) %>%

mutate(type = "Quadratic"),

epred_draws(laf_spln, newdata = tr_seq) %>%

median_qi(.width = c(0.67, 0.89, 0.97)) %>%

mutate(type = "Spline")

)

ggplot() +

facet_wrap(~type, nrow = 1) +

geom_ribbon(data = predictions,

aes(x = tax_rate, ymin = .lower, ymax = .upper),

alpha = 0.2) +

geom_lineribbon(data = fits,

aes(x = tax_rate, y = .epred, ymin = .lower, ymax = .upper),

size = 0.6) +

geom_point(data = laf_dat, aes(x = tax_rate, y = tax_revenue),

alpha = 0.5) +

scale_fill_manual(values = ramp_blue(seq(0.9, 0.1, length.out = 3)),

breaks = c(0.67, 0.89, 0.97)) +

labs(x = "Standardized Tax Rate", y = "Standardized Tax Revenue",

fill = "Interval")

They all look pretty similar, but the quadratic and spline models do show a slight curve. Next, we can look at the PSIS (called LOO in {brms} and {rstan}) and WAIC comparisons. Neither the PSIS or WAIC is really able to differentiate the models in a meaningful way. However, it should be noted that both the PSIS and WAIC have Pareto or penalty values that are exceptionally large, which could make the criteria unreliable.

library(loo)

laf_line <- add_criterion(laf_line, criterion = c("loo", "waic"))

laf_quad <- add_criterion(laf_quad, criterion = c("loo", "waic"))

laf_spln <- add_criterion(laf_spln, criterion = c("loo", "waic"))

loo_compare(laf_line, laf_quad, laf_spln, criterion = "waic")

#> elpd_diff se_diff

#> laf_quad 0.0 0.0

#> laf_spln -0.1 0.6

#> laf_line -0.9 0.9

loo_compare(laf_line, laf_quad, laf_spln, criterion = "loo")

#> elpd_diff se_diff

#> laf_spln 0.0 0.0

#> laf_quad 0.0 0.7

#> laf_line -0.8 0.97H2. In the

Lafferdata, there is one country with a high tax revenue that is an outlier. Use PSIS and WAIC to measure the importance of this outlier in the models you fit in the previous problem. Then use robust regression with a Student’s t distribution to revist the curve fitting problem. How much does a curved relationship depend upon the outlier point.

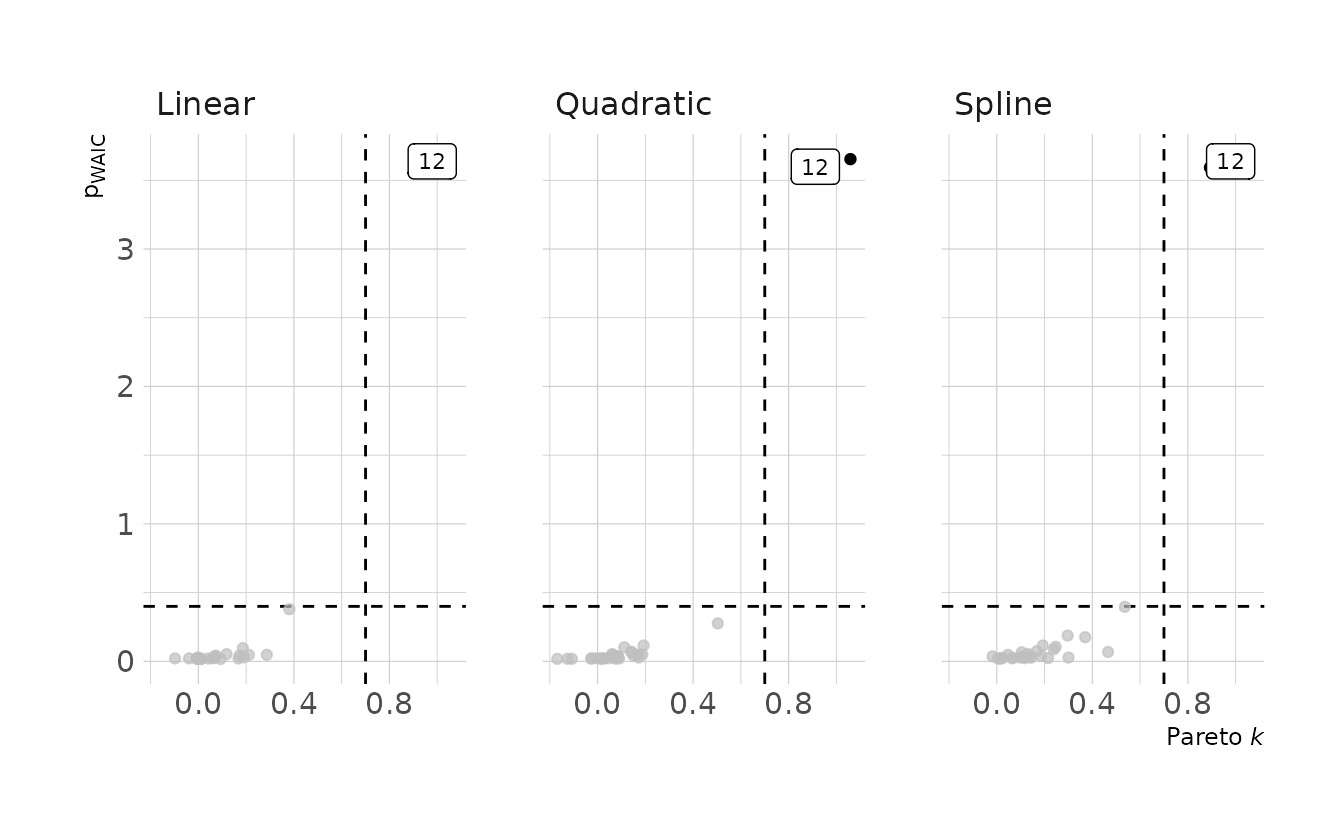

Because I used brms::brm() to estimate the models, we can’t use the convenience functions to get the pointwise values for the PSIS and WAIC that are available in the {rethinking} package. So I’ll write my own, called criteria_influence(). When we plot the Pareto k and \(p_{\Tiny\text{WAIC}}\) values, we see that observation 12 is problematic in all three models.

library(gghighlight)

criteria_influence <- function(mod) {

tibble(pareto_k = mod$criteria$loo$diagnostics$pareto_k,

p_waic = mod$criteria$waic$pointwise[, "p_waic"]) %>%

rowid_to_column(var = "obs")

}

influ <- bind_rows(

criteria_influence(laf_line) %>%

mutate(type = "Linear"),

criteria_influence(laf_quad) %>%

mutate(type = "Quadratic"),

criteria_influence(laf_spln) %>%

mutate(type = "Spline")

)

ggplot(influ, aes(x = pareto_k, y = p_waic)) +

facet_wrap(~type, nrow = 1) +

geom_vline(xintercept = 0.7, linetype = "dashed") +

geom_hline(yintercept = 0.4, linetype = "dashed") +

geom_point() +

gghighlight(pareto_k > 0.7 | p_waic > 0.4, n = 1, label_key = obs,

label_params = list(size = 3)) +

labs(x = "Pareto *k*", y = "p<sub>WAIC</sub>")

Let’s refit the model using a Student’s t distribution to put larger tails on our outcome distribution, and then visualize our new models.

laf_line2 <- brm(bf(tax_revenue ~ 1 + tax_rate, nu = 1),

data = laf_dat, family = student,

prior = c(prior(normal(0, 0.2), class = Intercept),

prior(normal(0, 0.5), class = b),

prior(exponential(1), class = sigma)),

iter = 4000, warmup = 2000, chains = 4, cores = 4, seed = 1234,

file = here("fits", "chp7", "b7h2-line.rds"))

laf_quad2 <- brm(bf(tax_revenue ~ 1 + tax_rate + tax_rate2, nu = 1),

data = laf_dat, family = student,

prior = c(prior(normal(0, 0.2), class = Intercept),

prior(normal(0, 0.5), class = b),

prior(exponential(1), class = sigma)),

iter = 4000, warmup = 2000, chains = 4, cores = 4, seed = 1234,

file = here("fits", "chp7", "b7h2-quad.rds"))

laf_spln2 <- brm(bf(tax_revenue ~ 1 + s(tax_rate, bs = "bs"), nu = 1),

data = laf_dat, family = student,

prior = c(prior(normal(0, 0.2), class = Intercept),

prior(normal(0, 0.5), class = b),

prior(normal(0, 0.5), class = sds),

prior(exponential(1), class = sigma)),

iter = 4000, warmup = 2000, chains = 4, cores = 4, seed = 1234,

control = list(adapt_delta = 0.99),

file = here("fits", "chp7", "bh72-spln.rds"))Code to reproduce

predictions <- bind_rows(

predicted_draws(laf_line2, newdata = tr_seq) %>%

median_qi(.width = 0.89) %>%

mutate(type = "Linear"),

predicted_draws(laf_quad2, newdata = tr_seq) %>%

median_qi(.width = 0.89) %>%

mutate(type = "Quadratic"),

predicted_draws(laf_spln2, newdata = tr_seq) %>%

median_qi(.width = 0.89) %>%

mutate(type = "Spline")

)

fits <- bind_rows(

epred_draws(laf_line2, newdata = tr_seq) %>%

median_qi(.width = c(0.67, 0.89, 0.97)) %>%

mutate(type = "Linear"),

epred_draws(laf_quad2, newdata = tr_seq) %>%

median_qi(.width = c(0.67, 0.89, 0.97)) %>%

mutate(type = "Quadratic"),

epred_draws(laf_spln2, newdata = tr_seq) %>%

median_qi(.width = c(0.67, 0.89, 0.97)) %>%

mutate(type = "Spline")

)

ggplot() +

facet_wrap(~type, nrow = 1) +

geom_ribbon(data = predictions,

aes(x = tax_rate, ymin = .lower, ymax = .upper),

alpha = 0.2) +

geom_lineribbon(data = fits,

aes(x = tax_rate, y = .epred, ymin = .lower, ymax = .upper),

size = 0.6) +

geom_point(data = laf_dat, aes(x = tax_rate, y = tax_revenue),

alpha = 0.5) +

scale_fill_manual(values = ramp_blue(seq(0.9, 0.1, length.out = 3)),

breaks = c(0.67, 0.89, 0.97)) +

labs(x = "Standardized Tax Rate", y = "Standardized Tax Revenue",

fill = "Interval")

The prediction intervals are a little bit narrower, which makes sense as the predictions are no longer being as influenced by the outlier. When we look at the new PSIS and WAIC estimates, we are no longer getting warning messages about large Pareto k values; however, we do still see warnings about large \(p_{\Tiny\text{WAIC}}\) values. The comparisons also tell the same story as before, with no distinguishable differences between the models.

laf_line2 <- add_criterion(laf_line2, criterion = c("loo", "waic"))

laf_quad2 <- add_criterion(laf_quad2, criterion = c("loo", "waic"))

laf_spln2 <- add_criterion(laf_spln2, criterion = c("loo", "waic"))

loo_compare(laf_line2, laf_quad2, laf_spln2, criterion = "waic")

#> elpd_diff se_diff

#> laf_quad2 0.0 0.0

#> laf_spln2 -0.3 1.3

#> laf_line2 -1.1 1.7

loo_compare(laf_line2, laf_quad2, laf_spln2, criterion = "loo")

#> elpd_diff se_diff

#> laf_quad2 0.0 0.0

#> laf_spln2 -0.2 1.2

#> laf_line2 -1.1 1.77H3. Consider three fictional Polynesian islands. On each there is a Royal Ornithologist charged by the king with surveying the bird population. They have each found the following proportions of 5 important bird species:

| Species A | Species B | Species C | Species D | Species E | |

|---|---|---|---|---|---|

| Island 1 | 0.200 | 0.200 | 0.200 | 0.200 | 0.200 |

| Island 2 | 0.800 | 0.100 | 0.050 | 0.025 | 0.025 |

| Island 3 | 0.050 | 0.150 | 0.700 | 0.050 | 0.050 |

Notice that each row sums to 1, all the birds. This problem has two parts. It is not computationally complicated. But it is conceptually tricky. First, compute the entropy of each island’s bird distribution. Interpret these entropy values. Second, use each island’s bird distribution to predict the other two. This means to compute the KL divergence of each island from the others, treating each island as if it were a statistical model of the other islands. You should end up with 6 different KL divergence values. Which island predicts the others best? Why?

First, lets compute the entropy for each each island.

islands <- tibble(island = paste("Island", 1:3),

a = c(0.2, 0.8, 0.05),

b = c(0.2, 0.1, 0.15),

c = c(0.2, 0.05, 0.7),

d = c(0.2, 0.025, 0.05),

e = c(0.2, 0.025, 0.05)) %>%

pivot_longer(-island, names_to = "species", values_to = "prop")

islands %>%

group_by(island) %>%

summarize(prop = list(prop), .groups = "drop") %>%

mutate(entropy = map_dbl(prop, calc_entropy))

#> # A tibble: 3 × 3

#> island prop entropy

#> <chr> <list> <dbl>

#> 1 Island 1 <dbl [5]> 1.61

#> 2 Island 2 <dbl [5]> 0.743

#> 3 Island 3 <dbl [5]> 0.984The first island has the highest entropy. This is expected, because it has the most even distribution of bird species. All species are equally likely, so the observation of any one species is not surprising. In contrast, Island 2 has the lowest entropy. This is because the vast majority of birds on this island are Species A. Therefore, observing a bird that is not from Species A would be surprising.

For the second part of the question, we need to compute the KL divergence for each pair of islands. The KL divergence is defined as:

\[ D_{KL} = \sum_i p_i(\log(p_i) - \log(q_i)) \]

We’ll write a function to do this calculation.

Now, let’s calculate \(D_{KL}\) for each set of islands.

crossing(model = paste("Island", 1:3),

predicts = paste("Island", 1:3)) %>%

filter(model != predicts) %>%

left_join(islands, by = c("model" = "island")) %>%

rename(model_prop = prop) %>%

left_join(islands, by = c("predicts" = "island", "species")) %>%

rename(predict_prop = prop) %>%

group_by(model, predicts) %>%

summarize(q = list(model_prop),

p = list(predict_prop),

.groups = "drop") %>%

mutate(kl_distance = map2_dbl(p, q, d_kl))

#> # A tibble: 6 × 5

#> model predicts q p kl_distance

#> <chr> <chr> <list> <list> <dbl>

#> 1 Island 1 Island 2 <dbl [5]> <dbl [5]> 0.866

#> 2 Island 1 Island 3 <dbl [5]> <dbl [5]> 0.626

#> 3 Island 2 Island 1 <dbl [5]> <dbl [5]> 0.970

#> 4 Island 2 Island 3 <dbl [5]> <dbl [5]> 1.84

#> 5 Island 3 Island 1 <dbl [5]> <dbl [5]> 0.639

#> 6 Island 3 Island 2 <dbl [5]> <dbl [5]> 2.01These results show us that when using Island 1 to predict Island 2, the KL divergence is about 0.87. When we use Island 1 to predict Island 3, the KL divergence is about 0.63, and so on. Overall, the distances are shorter when we used Island 1 as the model. This is because Island 1 has the highest entropy. Thus, we are less surprised by the other islands, so there’s a shorter distance. In contrast, Island 2 and Island 3 have very concentrated distributions, so predicting the other islands leads to more surprises, and therefore greater distances.

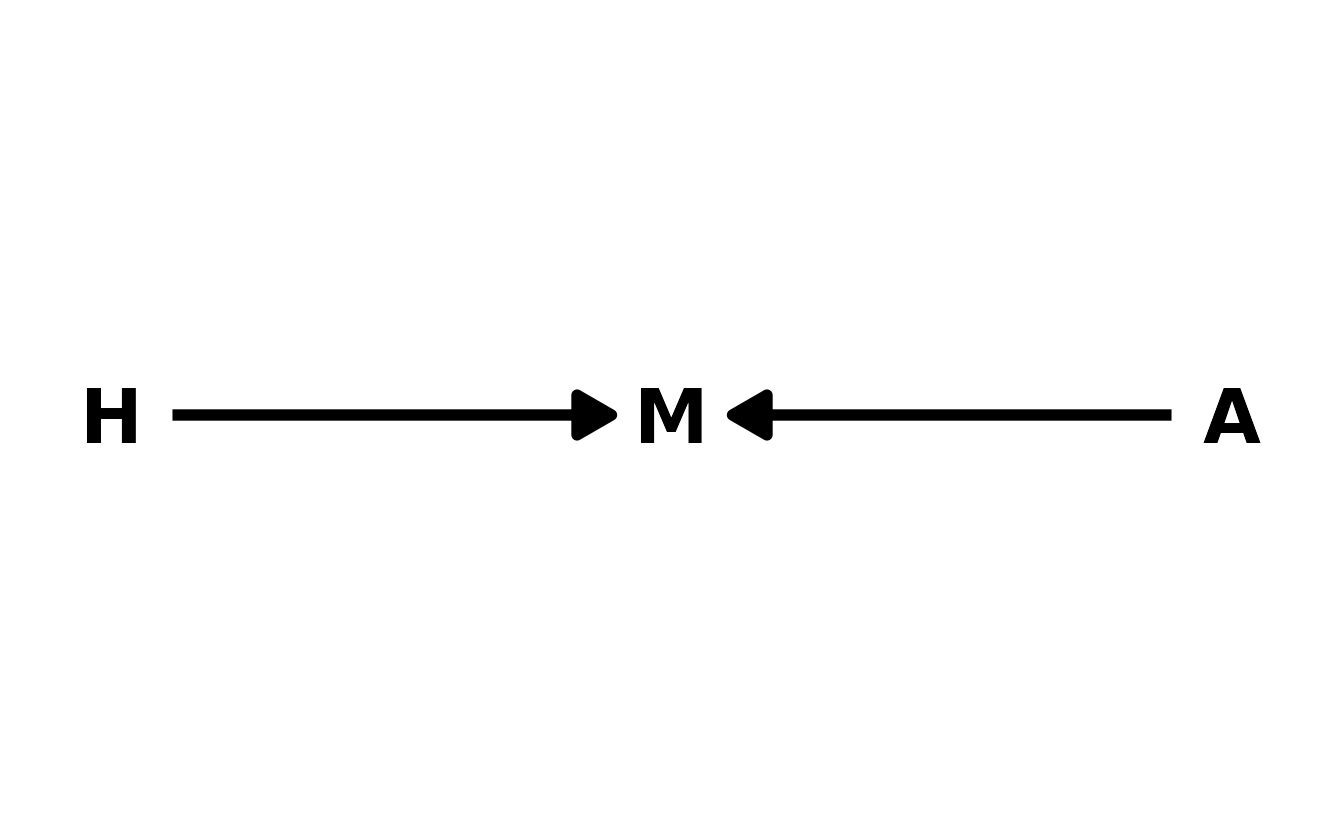

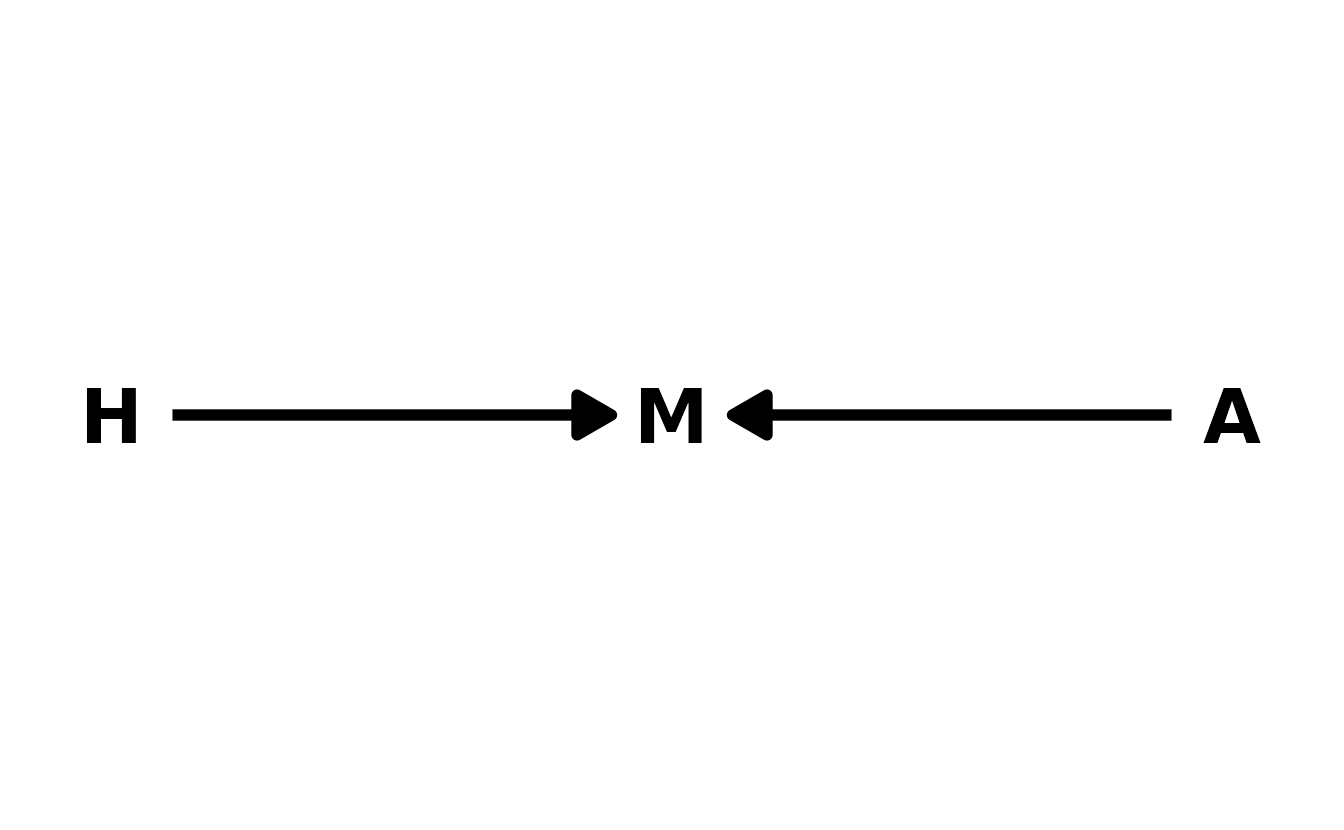

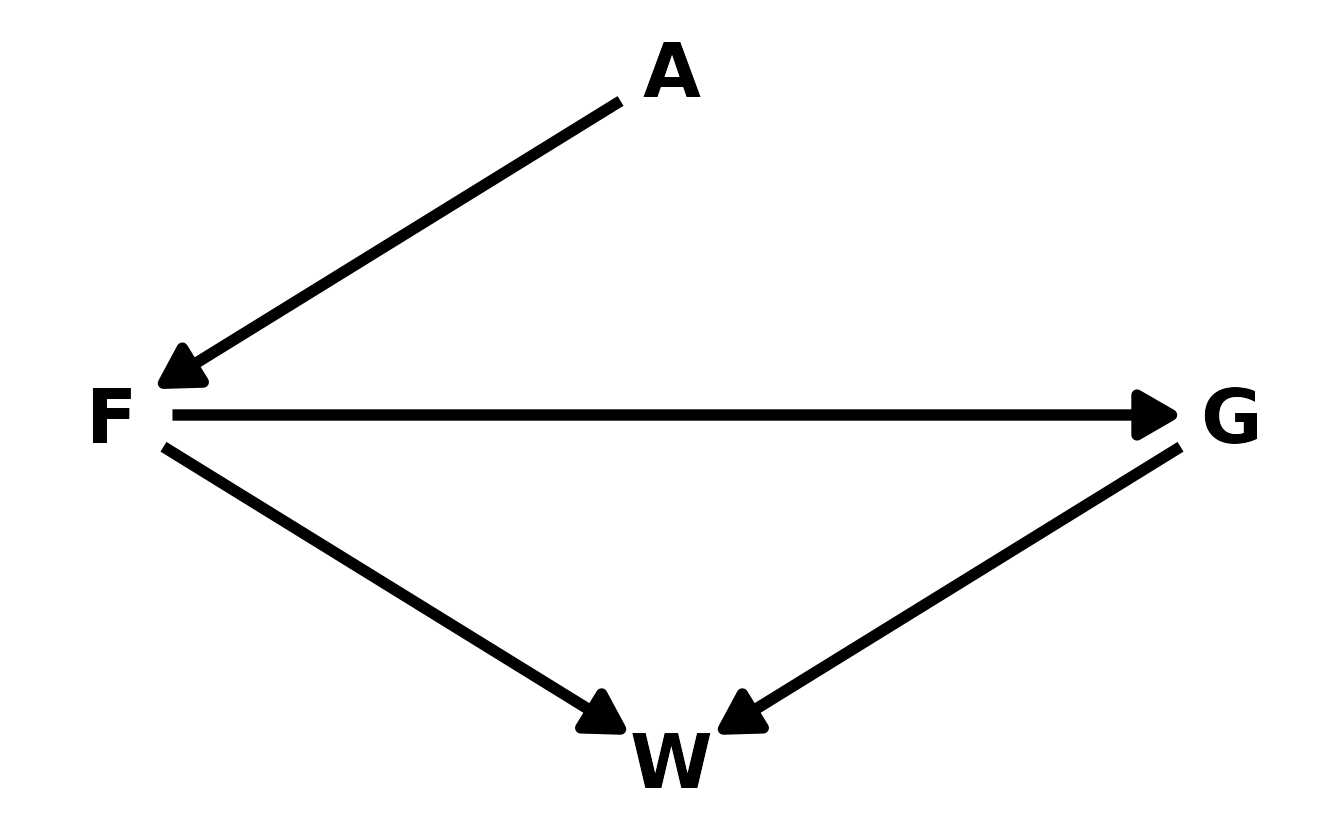

7H4. Recall the marriage, age, and happiness collider bias example from Chapter 6. Run models

m6.9andm6.10again (page 178). Compare these two models using WAIC (or PSIS, they will produce identical results). Which model is expected to make better predictions? Which model provides the correct causal inference about the influence of age on happiness? Can you explain why the answers to these two questions disagree?

As a reminder, here is the DAG for this example, where \(H\) is happiness, \(M\) is marriage, and \(A\) is age.

library(dagitty)

library(ggdag)

hma_dag <- dagitty("dag{H -> M <- A}")

coordinates(hma_dag) <- list(x = c(H = 1, M = 2, A = 3),

y = c(H = 1, M = 1, A = 1))

ggplot(hma_dag, aes(x = x, y = y, xend = xend, yend = yend)) +

geom_dag_text(color = "black", size = 10) +

geom_dag_edges(edge_color = "black", edge_width = 2,

arrow_directed = grid::arrow(length = grid::unit(15, "pt"),

type = "closed")) +

theme_void()

First, let’s regenerate the data and estimate the models.

d <- sim_happiness(seed = 1977, N_years = 1000)

dat <- d %>%

filter(age > 17) %>%

mutate(a = (age - 18) / (65 - 18),

mid = factor(married + 1, labels = c("single", "married")))

b6.9 <- brm(happiness ~ 0 + mid + a, data = dat, family = gaussian,

prior = c(prior(normal(0, 1), class = b, coef = midmarried),

prior(normal(0, 1), class = b, coef = midsingle),

prior(normal(0, 2), class = b, coef = a),

prior(exponential(1), class = sigma)),

iter = 4000, warmup = 2000, chains = 4, cores = 4, seed = 1234,

file = here("fits", "chp7", "b7h4-6.9"))

b6.10 <- brm(happiness ~ 1 + a, data = dat, family = gaussian,

prior = c(prior(normal(0, 1), class = Intercept),

prior(normal(0, 2), class = b, coef = a),

prior(exponential(1), class = sigma)),

iter = 4000, warmup = 2000, chains = 4, cores = 4, seed = 1234,

file = here("fits", "chp7", "b7h4-6.10"))For the model comparison we’ll use PSIS.

b6.9 <- add_criterion(b6.9, criterion = "loo")

b6.10 <- add_criterion(b6.10, criterion = "loo")

loo_compare(b6.9, b6.10)

#> elpd_diff se_diff

#> b6.9 0.0 0.0

#> b6.10 -194.0 17.6PSIS shows a strong preference for b6.9, which is the model that includes both age and marriage status. However, b6.10 provides the correct causal inference, as no additional conditioning is needed.

adjustmentSets(hma_dag, exposure = "A", outcome = "H")

#> {}The reason is that in this model, marital status is a collider. Adding this variable to the model add a real statistical association between happiness and age, which improves the predictions that are made. However, the association is not causal, so intervening on age (if that were possible), would not actually change happiness. Therefore it’s important to consider the causal implications of your model before selecting one based on PSIS or WAIC alone.

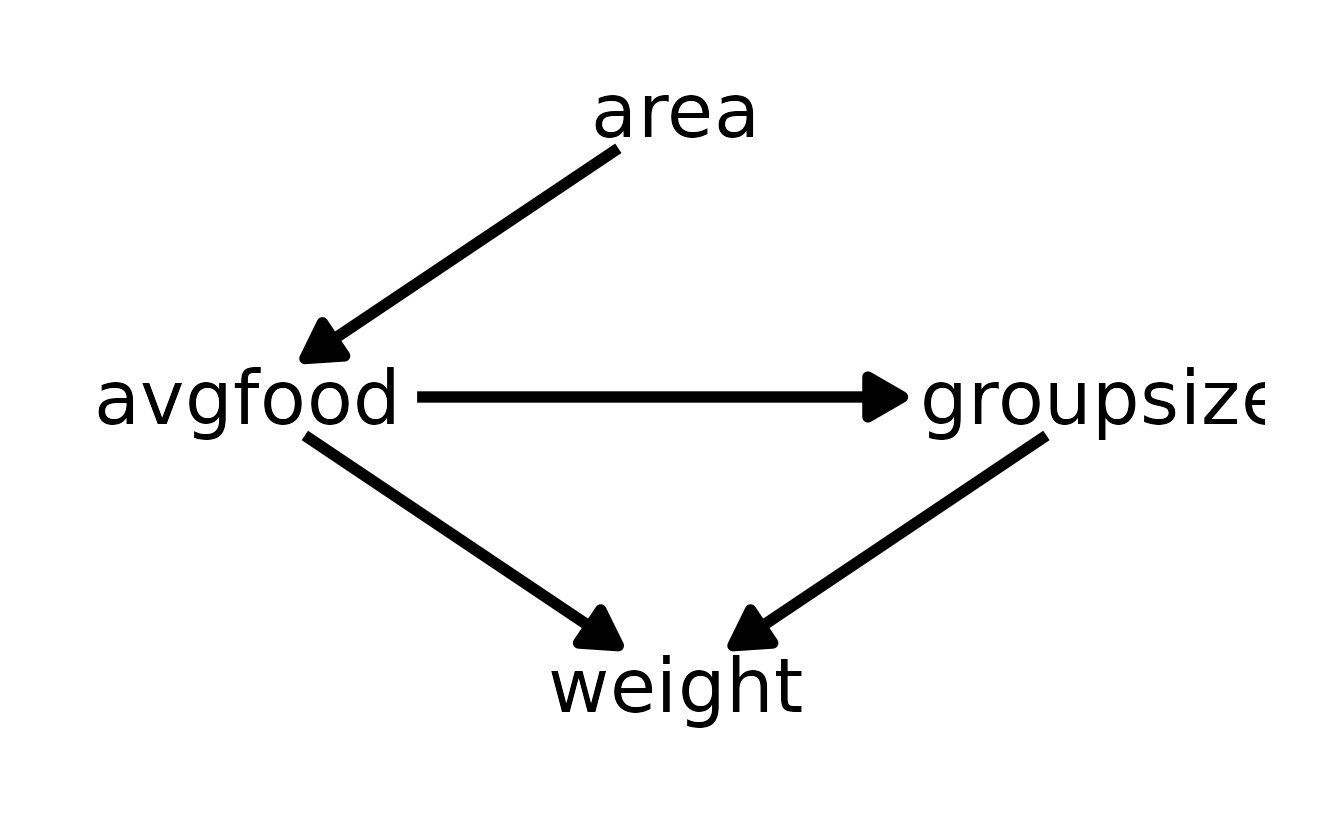

7H5. Revisit the urban fox data,

data(foxes), from the previous chapter’s practice problems. Use WAIC or PSIS based model comparison on five different models, each usingweightas the outcome, and containing these sets of predictor variables:

avgfood + groupsize + area

avgfood + groupsize

groupsize + area

avgfood

area

Can you explain the relative differences in WAIC scores, using the fox DAG from the previous chapter? Be sure to pay attention to the standard error of the score differences (

dSE).

First, let’s estimate the five models.

data(foxes)

fox_dat <- foxes %>%

as_tibble() %>%

select(area, avgfood, weight, groupsize) %>%

mutate(across(everything(), standardize))

b7h5_1 <- brm(weight ~ 1 + avgfood + groupsize + area, data = fox_dat,

family = gaussian,

prior = c(prior(normal(0, 0.2), class = Intercept),

prior(normal(0, 0.5), class = b),

prior(exponential(1), class = sigma)),

iter = 4000, warmup = 2000, chains = 4, cores = 4, seed = 1234,

file = here("fits", "chp7", "b7h5_1"))

b7h5_2 <- brm(weight ~ 1 + avgfood + groupsize, data = fox_dat,

family = gaussian,

prior = c(prior(normal(0, 0.2), class = Intercept),

prior(normal(0, 0.5), class = b),

prior(exponential(1), class = sigma)),

iter = 4000, warmup = 2000, chains = 4, cores = 4, seed = 1234,

file = here("fits", "chp7", "b7h5_2"))

b7h5_3 <- brm(weight ~ 1 + groupsize + area, data = fox_dat,

family = gaussian,

prior = c(prior(normal(0, 0.2), class = Intercept),

prior(normal(0, 0.5), class = b),

prior(exponential(1), class = sigma)),

iter = 4000, warmup = 2000, chains = 4, cores = 4, seed = 1234,

file = here("fits", "chp7", "b7h5_3"))

b7h5_4 <- brm(weight ~ 1 + avgfood, data = fox_dat,

family = gaussian,

prior = c(prior(normal(0, 0.2), class = Intercept),

prior(normal(0, 0.5), class = b),

prior(exponential(1), class = sigma)),

iter = 4000, warmup = 2000, chains = 4, cores = 4, seed = 1234,

file = here("fits", "chp7", "b7h5_4"))

b7h5_5 <- brm(weight ~ 1 + area, data = fox_dat,

family = gaussian,

prior = c(prior(normal(0, 0.2), class = Intercept),

prior(normal(0, 0.5), class = b),

prior(exponential(1), class = sigma)),

iter = 4000, warmup = 2000, chains = 4, cores = 4, seed = 1234,

file = here("fits", "chp7", "b7h5_5"))Then we can calculate the WAIC for each model and the model comparisons.

b7h5_1 <- add_criterion(b7h5_1, criterion = "waic")

b7h5_2 <- add_criterion(b7h5_2, criterion = "waic")

b7h5_3 <- add_criterion(b7h5_3, criterion = "waic")

b7h5_4 <- add_criterion(b7h5_4, criterion = "waic")

b7h5_5 <- add_criterion(b7h5_5, criterion = "waic")

comp <- loo_compare(b7h5_1, b7h5_2, b7h5_3, b7h5_4, b7h5_5, criterion = "waic")

comp

#> elpd_diff se_diff

#> b7h5_1 0.0 0.0

#> b7h5_3 -0.4 1.4

#> b7h5_2 -0.4 1.7

#> b7h5_4 -5.2 3.4

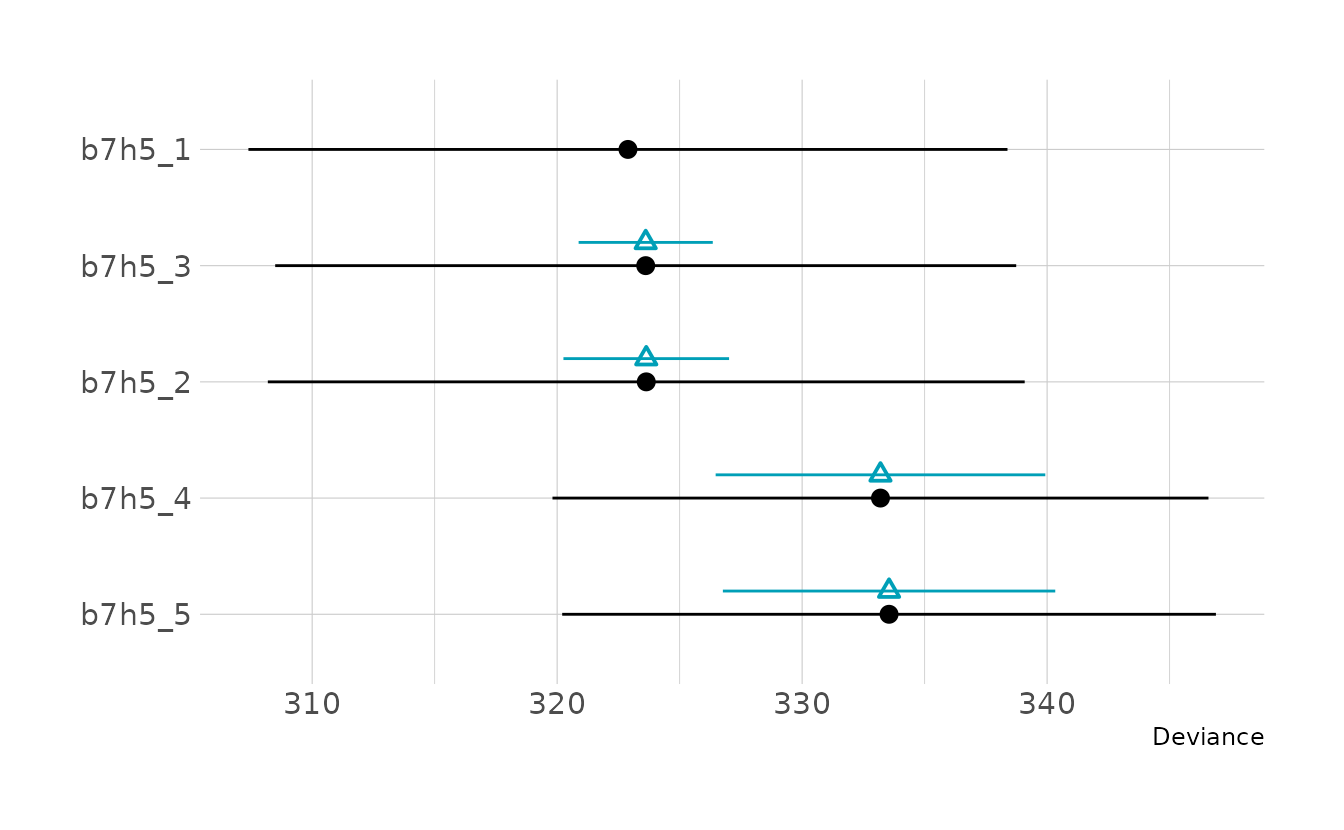

#> b7h5_5 -5.3 3.4In general, the models don’t appear all that different from each other. However, there does seem to be two groups of models: b7h5_1, b7h5_2, and b7h5_3 are all nearly identical; and b7h5_4 and b7h5_5 are nearly identical.

Code to reproduce

plot_comp <- comp %>%

as_tibble(rownames = "model") %>%

mutate(across(-model, as.numeric),

model = fct_inorder(model))

waic_val <- plot_comp %>%

select(model, waic, se = se_waic) %>%

mutate(lb = waic - se,

ub = waic + se)

diff_val <- plot_comp %>%

select(model, waic, se = se_diff) %>%

mutate(se = se * 2) %>%

mutate(lb = waic - se,

ub = waic + se) %>%

filter(se != 0)

ggplot() +

geom_pointrange(data = waic_val, mapping = aes(x = waic, xmin = lb, xmax = ub,

y = fct_rev(model))) +

geom_pointrange(data = diff_val, mapping = aes(x = waic, xmin = lb, xmax = ub,

y = fct_rev(model)),

position = position_nudge(y = 0.2), shape = 2,

color = "#009FB7") +

labs(x = "Deviance", y = NULL)

To understand why this is, we can return to the DAG for this example.

The first three models (b7h5_1, b7h5_2, and b7h5_3) all contain groupsize and one or both of area and avgfood. The reason these models is the same is that there are no back-door path from area or avgfood to weight. In other words, the effect of area adjusting for groupsize is the same as the effect of avgfood adjusting for groupsize, because the effect of area is routed entirely through avgfood.

Similarly, the last two models (b7h5_4 and b7h5_5) are also nearly identical because of the relationship of area to avgfood. Because the effect of area is routed entirely through avgfood, including only avgfood or area should result in the same inferences.

4.2.2 Chapter 8

8E1. For each of the causal relationships below, name a hypothetical third variable that would lead to an interaction effect.

- Bread dough rises because of yeast.

- Education leads to higher income.

- Gasoline makes a car go.

For the first, the amount of heat can moderate the relationship between yeast and the amount the dough rises. In the second example, ethnicity may give rise to an interaction, as individuals of some races face more systemic challenges (i.e., it’s easier for white people with low education to get a job than people of color). Thus, education may have more of an effect for minorities. Finally, a car also requires wheels. Wheels with no gas and gas with no wheels both prevent the car from moving; only with both will the car go.

8E2. Which of the following explanations invokes an interaction?

- Caramelizing onions requires cooking over low heat and making sure the onions do not dry out.

- A car will go faster when it has more cylinders or when it has better fuel injector.

- Most people acquire their political beliefs from their parents, unless they get them instead from their friends.

- Intelligent animal species tend to be either highly social or have manipulative appendages (hands, tentacles, etc.).

The first example is the only one that is, strictly speaking, an interaction. That is, low heat leads to camelization, conditional on the onions not drying out. In the second statement, it is phrased such that either more cylinders or a better fuel injector will result in faster speed. For number three, this is again phrased as an “or.” People acquire beliefs from their parents or their friends. As written, there is nothing to indicate that the influence of the parents’ beliefs depends on the influence of the friends’ beliefs (or vice versa). Finally, the last statement is also phrased as an “or.” There is no indicate that the influence of one factor impacts the influence of the other.

8E3. For each of the explanations in 8E2, write a linear model that expresses the stated relationship.

For onion caramelization, the mathematical model is:

\[ \begin{align} C_i &\sim \text{Normal}(\mu_i, \sigma) \\ \mu_i &= \alpha + \beta_HH_i + \beta_MM_i + \beta_{HM}H_iM_i \end{align} \]

The mathematical model for car speed is very similar:

\[ \begin{align} S_i &\sim \text{Normal}(\mu_i, \sigma) \\ \mu_i &= \alpha + \beta_CC_i + \beta_FF_i \end{align} \]

There is a similar model for political beliefs:

\[ \begin{align} B_i &\sim \text{Normal}(\mu_i, \sigma) \\ \mu_i &= \alpha + \beta_PP_i + \beta_FF_i \end{align} \]

And finally the model for intelligence:

\[ \begin{align} I_i &\sim \text{Normal}(\mu_i, \sigma) \\ \mu_i &= \alpha + \beta_SS_i + \beta_MM_i \end{align} \]

8M1. Recall the tulips example from the chapter. Suppose another set of treatments adjusted the temperature in the greenhouse over two levels: cold and hot. The data in the chapter were collected at the cold temperature. You find none of the plants grown under the hot temperature developed any blooms at all, regardless of the water and shade levels. Can you explain this result in terms of interactions between water, shade, and temperature?

In the chapter example, we saw that at cool temperatures, the blooms were best predicted by water, shade, and their interaction. Here, we learn that neither water nor light matter at a high temperature. This implies a three-way interaction. Just as in the chapter where water had no effect when there was no light, we see that neither water nor light have an effect when temperature is high.

8M2. Can you invent a regression equation that would make the bloom size zero, whenever the temperature is hot?

For this model, we can use the interaction model from the chapter with an additional predictor (\(C\)) that is 0 when the temperature is hot and 1 when the temperature is cold.

\[ \begin{align} B_i &\sim \text{Normal}(\mu_i, \sigma) \\ \mu_i &= C_i \times (\alpha + \beta_WW_i + \beta_SS_i + \beta_{WS}W_iS_i) \end{align} \]

8M3. In parts of North America, ravens depend upon wolves for their food. This is because ravens are carnivorous but cannot usually kill or open carcasses of prey. Wolves however can and do kill and tear open animals, and they tolerate ravens co-feeding at their kills. This species relationship is generally described as a “species interaction.” Can you invent a hypothetical set of data on raven population size in which this relationship would manifest as a statistical interaction? Do you think the biological interaction could be linear? Why or why not?

In order to predict raven population size based on wolf population size, we should include data on the territory area for the wolves, the number of wolves, and amount of food available, and finally the number of ravens. This is similar to the types of data included in data(foxes). I would expect the relationship to be non-linear. When there are no wolves, I would expect there to be no ravens. As the number of wolves increases, the number of ravens would also increase. However, eventually the number of wolves would increase to the point that the wolves exhaust the food supply, leaving no food left for the ravens, at which point the raven population would begin to shrink. Thus, if we created a counter factual plot with wolves on the x-axis and ravens on the y-axis, I would expect to see at linear trend at first, but then the raven population level off or drop when there is a large numbers of wolves.

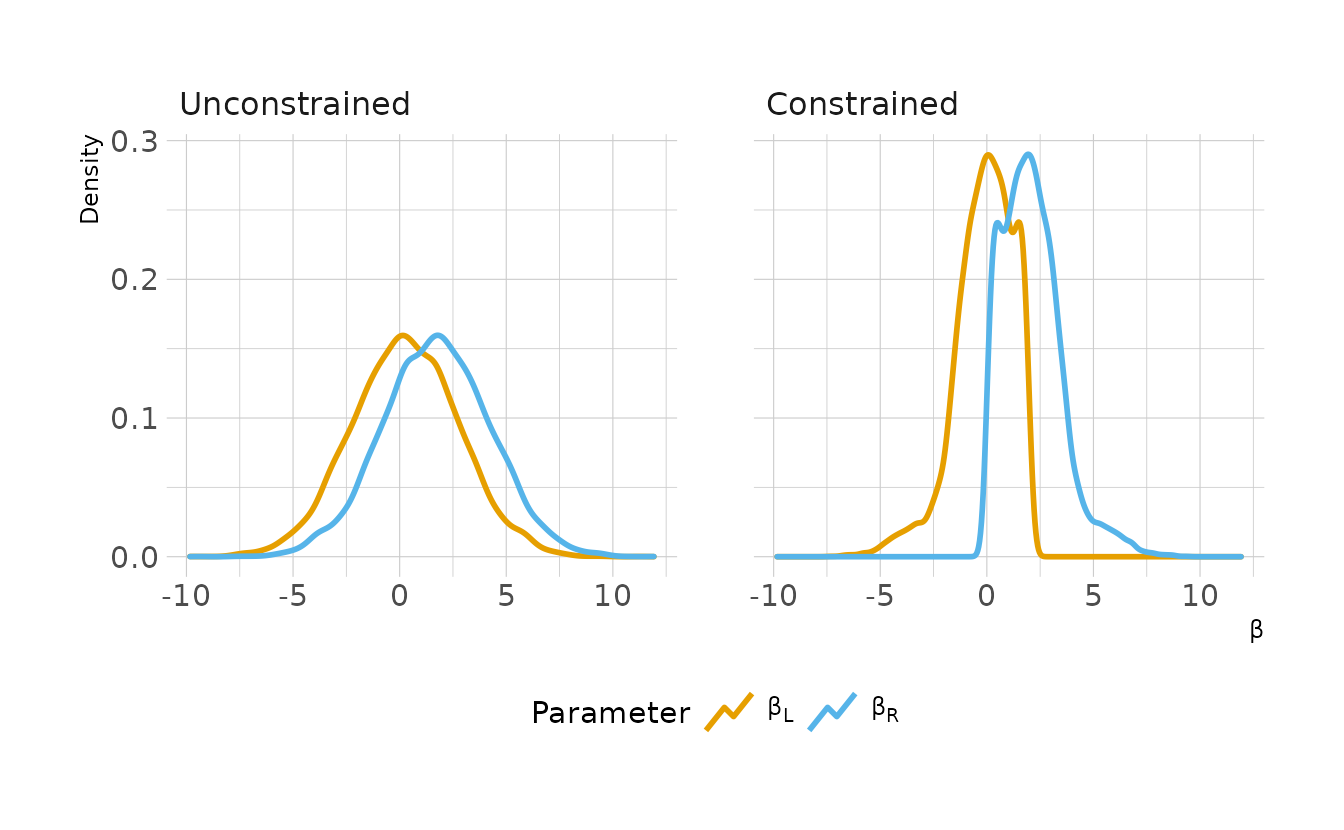

8M4. Repeat the tulips analysis, but this time use priors that constrain the effect of water to be positive and the effect of shade to be negative. Use prior predictive simulation. What do these prior asumptions mean for the interaction prior, if anything?

There are a few issues constraining different coefficients with bounded parameters (especially negative parameters) in {brms}. For some details, see this thread on the Stan discourse. To get around this, rather than constrain the shade parameter to be negative, we’ll create a new variable which is the opposite of shade, light and the corresponding light_cent. We can then constrain this parameter to be positive, just as the water_cent parameter is constrained to be positive. Finally, because of the new light variable the positivity constraints on the main effects, we also want to constrain the interaction term to be positive. That is, if both water and light increase, we expect an additional additive effect.

library(rethinking)

data("tulips")

tulip_dat <- tulips %>%

as_tibble() %>%

mutate(light = -1 * shade,

blooms_std = blooms / max(blooms),

water_cent = water - mean(water),

shade_cent = shade - mean(shade),

light_cent = light - mean(light))

b8m4 <- brm(blooms_std ~ 1 + water_cent + light_cent + water_cent:light_cent,

data = tulip_dat, family = gaussian,

prior = c(prior(normal(0.5, 0.25), class = Intercept),

prior(normal(0, 0.25), class = b, lb = 0),

prior(exponential(1), class = sigma)),

iter = 4000, warmup = 2000, chains = 4, cores = 4, seed = 1234,

file = here("fits", "chp8", "b8m4"))

summary(b8m4)

#> Family: gaussian

#> Links: mu = identity; sigma = identity

#> Formula: blooms_std ~ 1 + water_cent + light_cent + water_cent:light_cent

#> Data: tulip_dat (Number of observations: 27)

#> Draws: 4 chains, each with iter = 2000; warmup = 0; thin = 1;

#> total post-warmup draws = 8000

#>

#> Population-Level Effects:

#> Estimate Est.Error l-95% CI u-95% CI Rhat Bulk_ESS

#> Intercept 0.36 0.03 0.30 0.41 1.00 7951

#> water_cent 0.21 0.03 0.14 0.27 1.00 7826

#> light_cent 0.11 0.03 0.04 0.18 1.00 5064

#> water_cent:light_cent 0.14 0.04 0.06 0.22 1.00 7552

#> Tail_ESS

#> Intercept 5632

#> water_cent 4256

#> light_cent 2627

#> water_cent:light_cent 3884

#>

#> Family Specific Parameters:

#> Estimate Est.Error l-95% CI u-95% CI Rhat Bulk_ESS Tail_ESS

#> sigma 0.14 0.02 0.11 0.20 1.00 5469 5185

#>

#> Draws were sampled using sample(hmc). For each parameter, Bulk_ESS

#> and Tail_ESS are effective sample size measures, and Rhat is the potential

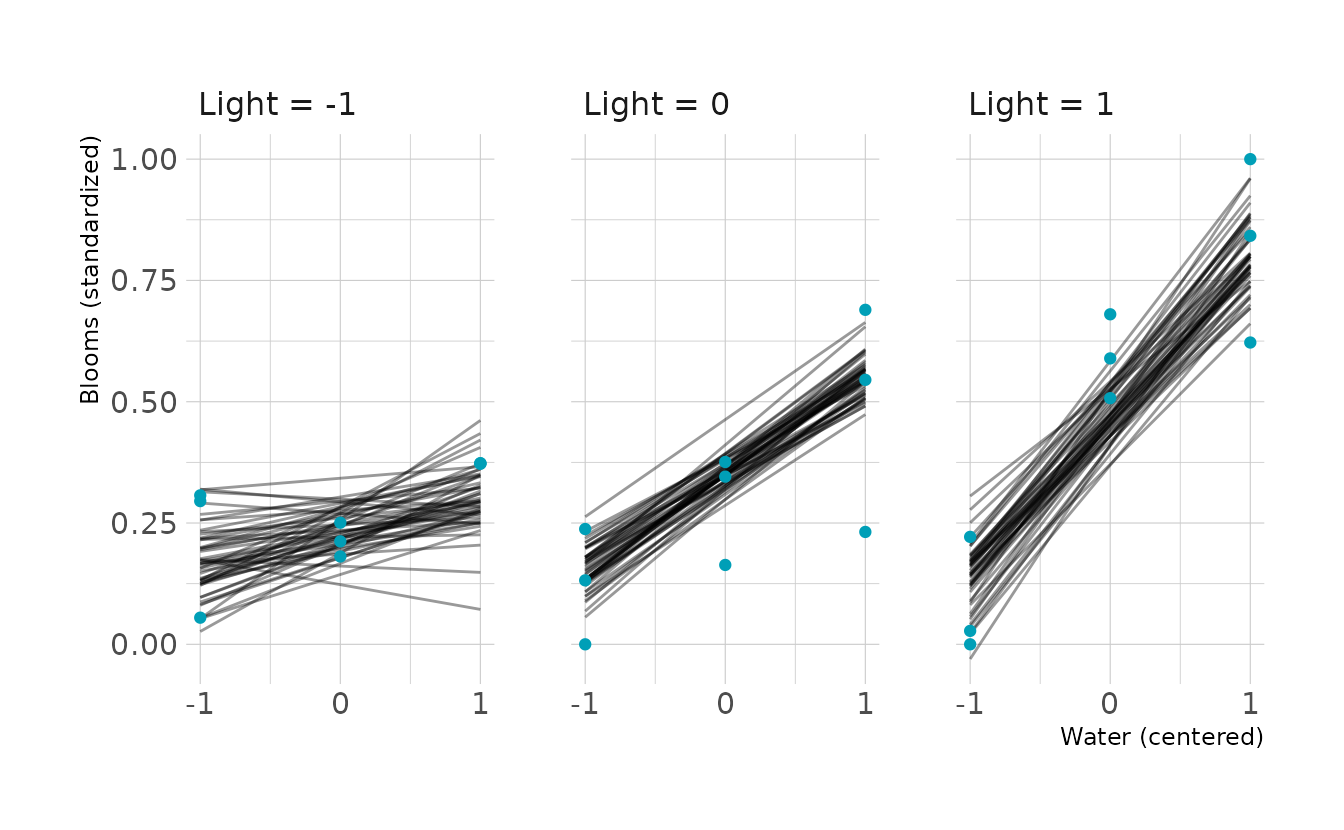

#> scale reduction factor on split chains (at convergence, Rhat = 1).Looking at the the posterior predicted blooms, the results are very similar to what we saw in Figure 8.7 from the text. This indicates that the prior constraints did not have a large effect on the predicted values.

new_tulip <- crossing(water_cent = -1:1,

light_cent = -1:1)

points <- tulip_dat %>%

expand(nesting(water_cent, light_cent, blooms_std)) %>%

mutate(light_grid = glue("light_cent = {light_cent}"))

to_string <- as_labeller(c(`-1` = "Light = -1", `0` = "Light = 0",

`1` = "Light = 1"))

new_tulip %>%

add_epred_draws(b8m4, ndraws = 50) %>%

ungroup() %>%

ggplot(aes(x = water_cent, y = .epred)) +

facet_wrap(~light_cent, nrow = 1,

labeller = to_string) +

geom_line(aes(group = .draw), alpha = 0.4) +

geom_point(data = points, aes(y = blooms_std), color = "#009FB7") +

scale_x_continuous(breaks = -1:1) +

labs(x = "Water (centered)", y = "Blooms (standardized)")

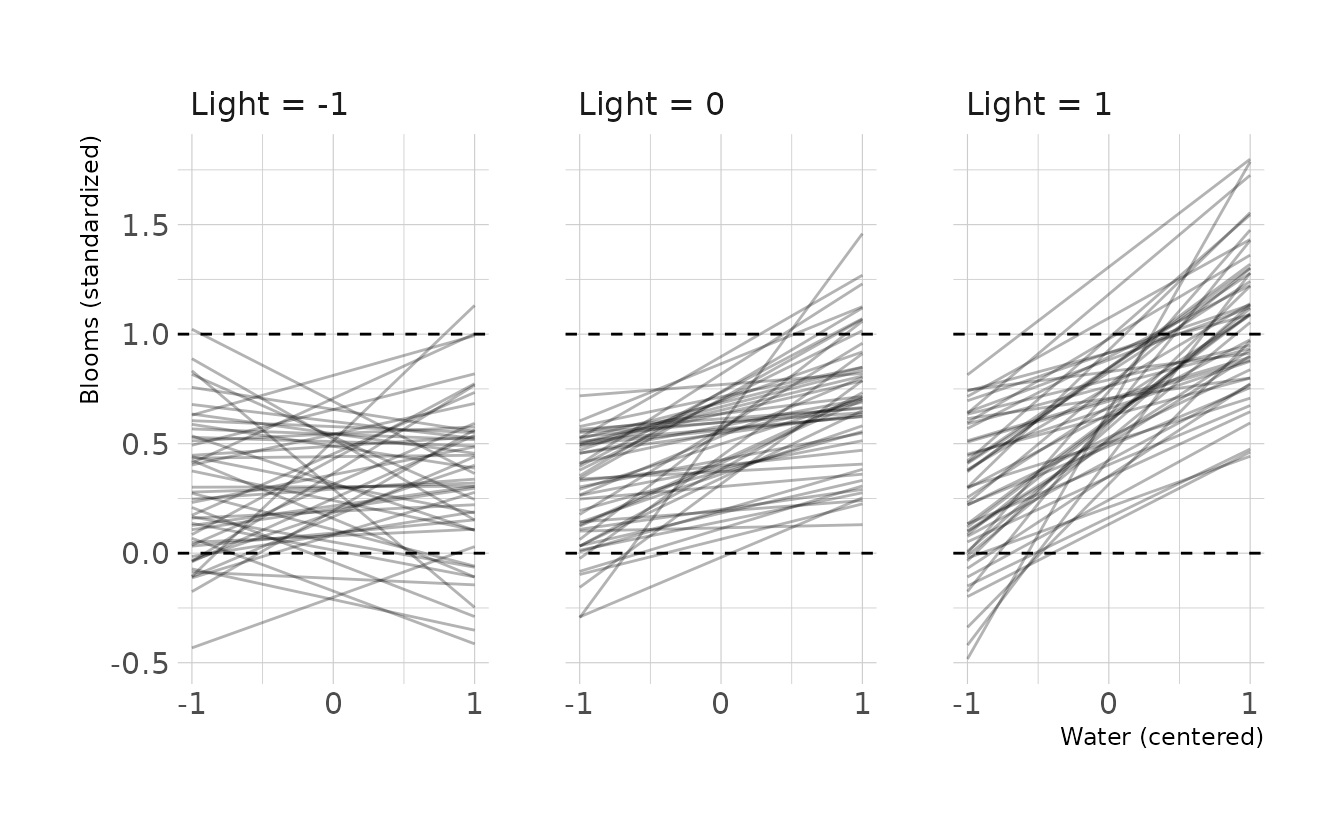

Finally, let’s look at the prior predictive simulation for this model. Overall the priors might be a little too uninformative, especially for the interaction. The interaction has the most impact in the far right panel of the below figure, and there are many lines that exceed the expected boundaries in this panel.

b8m4p <- update(b8m4, sample_prior = "only",

iter = 4000, warmup = 2000, chains = 4, cores = 4, seed = 1234,

file = here("fits", "chp8", "b8m4p.rds"))

#> The desired updates require recompiling the model

new_tulip %>%

add_epred_draws(b8m4p, ndraws = 50) %>%

ungroup() %>%

ggplot(aes(x = water_cent, y = .epred)) +

facet_wrap(~light_cent, nrow = 1,

labeller = to_string) +

geom_line(aes(group = .draw), alpha = 0.3) +

geom_hline(yintercept = c(0, 1), linetype = "dashed") +

scale_x_continuous(breaks = -1:1) +

labs(x = "Water (centered)", y = "Blooms (standardized)")

8H1. Return to the

data(tulips)example in the chapter. Now include thebedvariable as a predictor in the interaction model. Don’t interactbedwith the other predictors; just include it as a main effect. Note thatbedis categorical. So to use it properly, you will need to either construct dummy variables, or rather an index variable, as explained in Chapter 5.

The bed variable is already a factor variable in the tulips data, so we can just add it to the formula in brm(). To use indicator variables instead of a dummy variable, we remove the separate intercept (i.e., ~ 0 in the formula below). Because of what’s coming in the next question, we’ll use light instead of shade for this model also.

b8h1 <- brm(blooms_std ~ 0 + water_cent + light_cent + bed +

water_cent:light_cent,

data = tulip_dat, family = gaussian,

prior = c(prior(normal(0, 0.25), class = b),

prior(exponential(1), class = sigma)),

iter = 4000, warmup = 2000, chains = 4, cores = 4, seed = 1234,

file = here("fits", "chp8", "b8h1.rds"))

summary(b8h1)

#> Family: gaussian

#> Links: mu = identity; sigma = identity

#> Formula: blooms_std ~ 0 + water_cent + light_cent + bed + water_cent:light_cent

#> Data: tulip_dat (Number of observations: 27)

#> Draws: 4 chains, each with iter = 2000; warmup = 0; thin = 1;

#> total post-warmup draws = 8000

#>

#> Population-Level Effects:

#> Estimate Est.Error l-95% CI u-95% CI Rhat Bulk_ESS

#> water_cent 0.21 0.03 0.14 0.27 1.00 11367

#> light_cent 0.11 0.03 0.05 0.17 1.00 12221

#> beda 0.26 0.04 0.17 0.35 1.00 12912

#> bedb 0.38 0.04 0.29 0.47 1.00 12297

#> bedc 0.40 0.04 0.31 0.48 1.00 12459

#> water_cent:light_cent 0.14 0.04 0.07 0.22 1.00 12903

#> Tail_ESS

#> water_cent 6156

#> light_cent 6045

#> beda 5953

#> bedb 5615

#> bedc 5556

#> water_cent:light_cent 6107

#>

#> Family Specific Parameters:

#> Estimate Est.Error l-95% CI u-95% CI Rhat Bulk_ESS Tail_ESS

#> sigma 0.13 0.02 0.10 0.18 1.00 6707 5592

#>

#> Draws were sampled using sample(hmc). For each parameter, Bulk_ESS

#> and Tail_ESS are effective sample size measures, and Rhat is the potential

#> scale reduction factor on split chains (at convergence, Rhat = 1).8H2. Use WAIC to compare the model from 8H1 to a model that omits

bed. What do you infer from this comparison? Can you reconcile the WAIC results with the posterior distribution of thebedcoefficients?

For the comparison, we’ll compare b8h1 to the model b8m4, which is the model from the chapter, with new prior distributions that constrain the main effect of water to be positive and the main effect of shade to be negative (i.e., the main effect of light is positive).

Model b8h1 is the preferred model; however, the standard error of the difference is larger than the magnitude of the difference, indicating that the WAIC is not able to meaningfully differentiate between the two models. For predictive purposes, this means that the inclusion of the bed variable does not significantly improve the model. It should also be noted that both of the models have some exceptionally large penalty values, so these analyses may be unreliable, and we should consider re-fitting the models with a distribution with fatter tails.

b8m4 <- add_criterion(b8m4, criterion = "waic")

b8h1 <- add_criterion(b8h1, criterion = "waic")

loo_compare(b8m4, b8h1, criterion = "waic") %>%

print(simplify = FALSE)

#> elpd_diff se_diff elpd_waic se_elpd_waic p_waic se_p_waic waic se_waic

#> b8h1 0.0 0.0 13.7 3.3 6.2 1.4 -27.3 6.6

#> b8m4 -1.2 3.0 12.5 3.8 4.3 1.1 -24.9 7.68H3. Consider again the

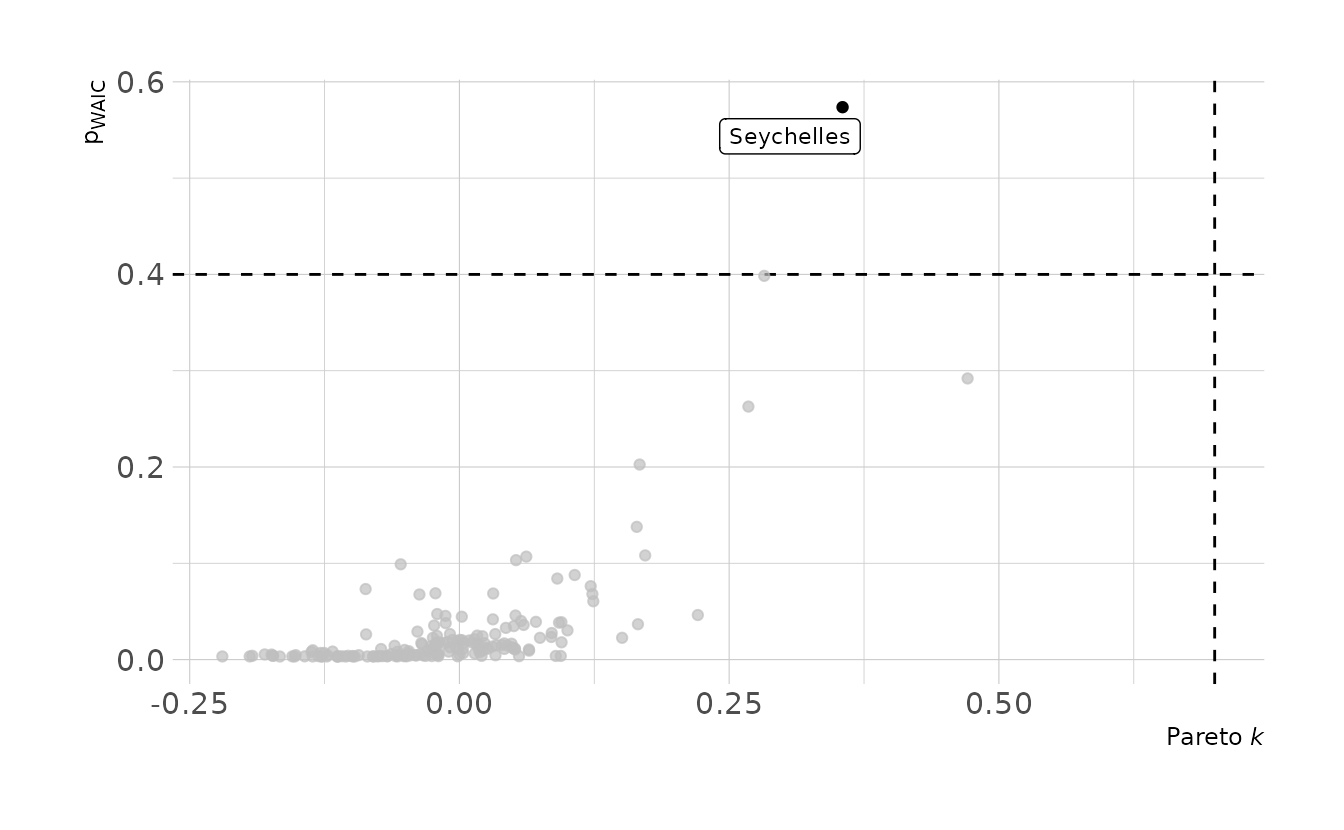

data(rugged)data on economic development and terrain ruggedness, examined in this chapter. One of the African countries in that example Seychelles, is far outside the cloud of other nations, being a rare country with both relatively high GDP and high ruggedness. Seychelles is also unusual, in that it is a group of islands far from the coast of mainland Africa, and its main economic activity is tourism.

- Focus on model

m8.5from the chapter. Use WAIC pointwise penalties and PSIS Pareto k values to measure relative influence of each country. By these criteria, is Seychelles influencing the results? Are there other nations that are relatively influential? If so, can you explain why?- Now use robust regression, as described in the previous chapter. Modify

m8.5to se a Student-t distribution with \(\nu = 2\). Does this change the results in a substantial way?

In the text, model m8.5 uses the tulips data, so I’m assuming this is a typo and we should be looking at model m8.3, which is the interaction model from the terrain ruggedness example in the chapter. So, let’s first create a {brms} version of model m8.3.

data("rugged")

rugged_dat <- rugged %>%

as_tibble() %>%

select(country, rgdppc_2000, rugged, cont_africa) %>%

drop_na(rgdppc_2000) %>%

mutate(log_gdp = log(rgdppc_2000),

log_gdp_std = log_gdp / mean(log_gdp),

rugged_std = rugged / max(rugged),

rugged_std_cent = rugged_std - mean(rugged_std),

cid = factor(cont_africa, levels = c(1, 0),

labels = c("African", "Not African")))

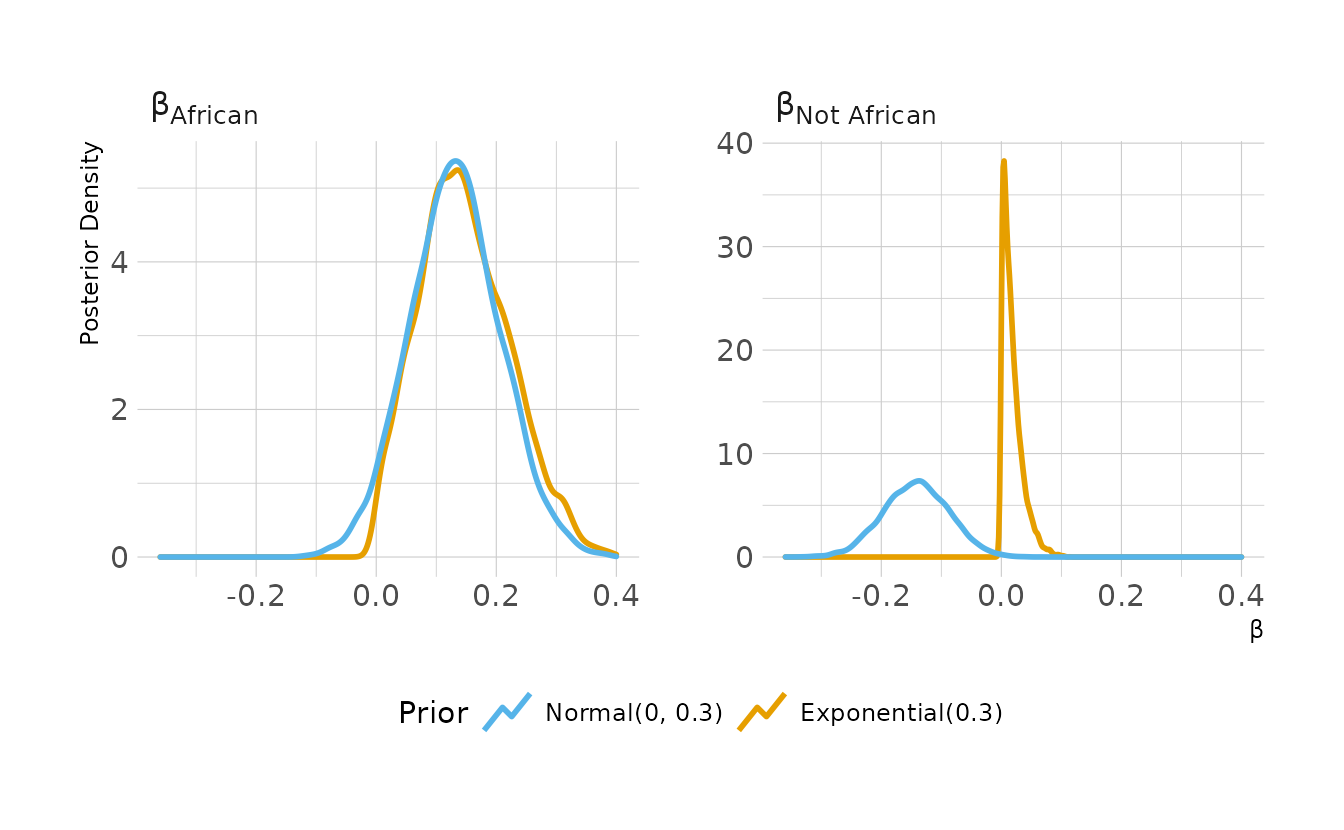

b8h3 <- brm(

bf(log_gdp_std ~ 0 + a + b * rugged_std_cent,

a ~ 0 + cid,

b ~ 0 + cid,

nl = TRUE),

data = rugged_dat, family = gaussian,

prior = c(prior(normal(1, 0.1), class = b, coef = cidAfrican, nlpar = a),

prior(normal(1, 0.1), class = b, coef = cidNotAfrican, nlpar = a),

prior(normal(0, 0.3), class = b, coef = cidAfrican, nlpar = b),

prior(normal(0, 0.3), class = b, coef = cidNotAfrican, nlpar = b),

prior(exponential(1), class = sigma)),

iter = 4000, warmup = 2000, chains = 4, cores = 4, seed = 1234,

file = here("fits", "chp8", "b8h3.rds")

)

b8h3 <- add_criterion(b8h3, criterion = c("loo", "waic"))

summary(b8h3)

#> Family: gaussian

#> Links: mu = identity; sigma = identity

#> Formula: log_gdp_std ~ 0 + a + b * rugged_std_cent

#> a ~ 0 + cid

#> b ~ 0 + cid

#> Data: rugged_dat (Number of observations: 170)

#> Draws: 4 chains, each with iter = 2000; warmup = 0; thin = 1;

#> total post-warmup draws = 8000

#>

#> Population-Level Effects:

#> Estimate Est.Error l-95% CI u-95% CI Rhat Bulk_ESS Tail_ESS

#> a_cidAfrican 0.89 0.02 0.85 0.92 1.00 9876 6334

#> a_cidNotAfrican 1.05 0.01 1.03 1.07 1.00 10083 6572

#> b_cidAfrican 0.13 0.08 -0.02 0.28 1.00 9543 6356

#> b_cidNotAfrican -0.14 0.05 -0.25 -0.04 1.00 9485 6149

#>

#> Family Specific Parameters:

#> Estimate Est.Error l-95% CI u-95% CI Rhat Bulk_ESS Tail_ESS

#> sigma 0.11 0.01 0.10 0.12 1.00 8960 6057

#>

#> Draws were sampled using sample(hmc). For each parameter, Bulk_ESS

#> and Tail_ESS are effective sample size measures, and Rhat is the potential

#> scale reduction factor on split chains (at convergence, Rhat = 1).Now let’s take a look at the Pareto k and \(p_{\Tiny\text{WAIC}}\) values from the model. Seychelles does appear to be influential. The Pareto \(k\) value is not above the above the 0.7 threshold; however, the \(p_{\Tiny\text{WAIC}}\) value is above the 0.4 threshold. No other countries have Pareto k or \(p_{\Tiny\text{WAIC}}\) values over the thresholds.

library(gghighlight)

tibble(pareto_k = b8h3$criteria$loo$diagnostics$pareto_k,

p_waic = b8h3$criteria$waic$pointwise[, "p_waic"]) %>%

rowid_to_column(var = "obs") %>%

left_join(rugged_dat %>%

select(country) %>%

rowid_to_column(var = "obs"),

by = "obs") %>%

ggplot(aes(x = pareto_k, y = p_waic)) +

geom_vline(xintercept = 0.7, linetype = "dashed") +

geom_hline(yintercept = 0.4, linetype = "dashed") +

geom_point() +

gghighlight(pareto_k > 0.7 | p_waic > 0.4, n = 1, label_key = country,

label_params = list(size = 3)) +

labs(x = "Pareto *k*", y = "p<sub>WAIC</sub>")

Now for part (b), we’ll use a Student-t distribution with \(\nu = 2\).

b8h3_t <- brm(

bf(log_gdp_std ~ 0 + a + b * rugged_std_cent,

a ~ 0 + cid,

b ~ 0 + cid,

nu = 2,

nl = TRUE),

data = rugged_dat, family = student,

prior = c(prior(normal(1, 0.1), class = b, coef = cidAfrican, nlpar = a),

prior(normal(1, 0.1), class = b, coef = cidNotAfrican, nlpar = a),

prior(normal(0, 0.3), class = b, coef = cidAfrican, nlpar = b),

prior(normal(0, 0.3), class = b, coef = cidNotAfrican, nlpar = b),

prior(exponential(1), class = sigma)),

iter = 4000, warmup = 2000, chains = 4, cores = 4, seed = 1234,

file = here("fits", "chp8", "b8h3_t.rds")

)

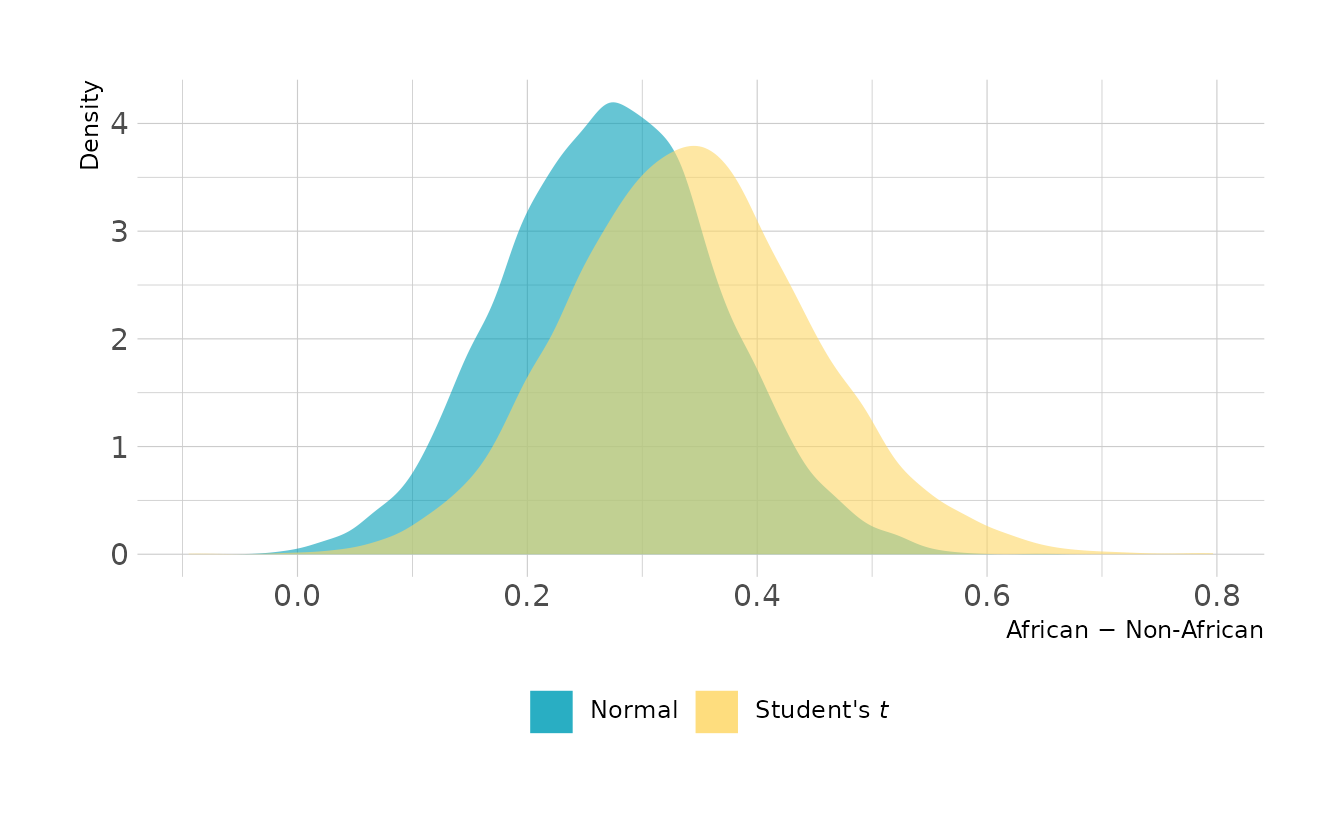

b8h3_t <- add_criterion(b8h3_t, criterion = c("loo", "waic"))How much does the Student’s t distribution affect our model? Let’s look at the posterior distribution of the difference between African and Non-African countries. In the Student’s t model, the difference actually increased on average. This is because switching the distribution affects all points, not just the high leverage points that were flagged originally. Therefore, it’s not unexpected that the distribution might shift.

n_diff <- spread_draws(b8h3, b_b_cidAfrican, b_b_cidNotAfrican) %>%

mutate(diff = b_b_cidAfrican - b_b_cidNotAfrican)

t_diff <- spread_draws(b8h3_t, b_b_cidAfrican, b_b_cidNotAfrican) %>%

mutate(diff = b_b_cidAfrican - b_b_cidNotAfrican)

ggplot() +

geom_density(data = n_diff, aes(x = diff, fill = "Normal"),

color = NA, alpha = 0.6) +

geom_density(data = t_diff, aes(x = diff, fill = "Student's *t*"),

color = NA, alpha = 0.6) +

scale_fill_manual(values = c("#009FB7", "#FED766")) +

labs(x = "African − Non-African", y = "Density", fill = NULL) +

theme(legend.text = element_markdown())

8H4. The values in

data(nettle)are data on language diversity in 74 nations.1 The meaning of each column is given below.

country: Name of the countrynum.lang: Number of recognized languages spokenarea: Area in square kilometersk.pop: Population, in thousandsnum.stations: Number of weather stations that provided data for the next two columnsmean.growing.season: Average length of growing season, in monthssd.growing.season: Standard deviation of length of growing season, in months

Use these data to evaluate the hypothesis that language diversity is partly a product of food security. The notion is that, in productive ecologies, people don’t need large social networks to buffer them against risk of food shortfalls. The means cultural groups can be smaller and more self-sufficient, leading to more languages per capita. Use the number of languages per capita as the outcome:

d$lang.per.cap <- d$num.lang / d$k.popUse the logarithm of this new variable as your regression outcome. (A count model would be better here, but you’ll learn those later, in Chapter 11.) This problem is open ended, allowing you to decide how you address the hypotheses and the uncertain advice the modeling provides. If you think you need to use WAIC anyplace, please do. If you think you need certain priors, argue for them. If you think you need to plot predictions in a certain way, please do. Just try to honestly evaluate the main effects of both

mean.growing.seasonandsd.growing.season, as well as their two-way interaction. Here are three parts to help.

- Evaluate the hypothesis that language diversity, as measured by

log(lang.per.cap), is positively associated with average length of the growing season,mean.growing.season. Considerlog(area)in your regression(s) as a covariate (not an interaction). Interpret your results.

First, let’s calculate some new variables we’ll need for these models. We’ll also go ahead and standardize everything to make setting the priors a little bit easier.

data(nettle)

nettle <- nettle %>%

as_tibble() %>%

mutate(lang_per_cap = num.lang / k.pop,

log_lang_per_cap = log(lang_per_cap),

log_area = log(area),

lang_per_cap_std = standardize(log_lang_per_cap),

area_std = standardize(log_area),

mean_growing_std = standardize(mean.growing.season),

sd_growing_std = standardize(sd.growing.season))

nettle

#> # A tibble: 74 × 14

#> country num.lang area k.pop num.stations mean.growing.se… sd.growing.seas…

#> <fct> <int> <int> <int> <int> <dbl> <dbl>

#> 1 Algeria 18 2.38e6 25660 102 6.6 2.29

#> 2 Angola 42 1.25e6 10303 50 6.22 1.87

#> 3 Austra… 234 7.71e6 17336 134 6 4.17

#> 4 Bangla… 37 1.44e5 118745 20 7.4 0.73

#> 5 Benin 52 1.13e5 4889 7 7.14 0.99

#> 6 Bolivia 38 1.10e6 7612 48 6.92 2.5

#> 7 Botswa… 27 5.82e5 1348 10 4.6 1.69

#> 8 Brazil 209 8.51e6 153322 245 9.71 5.87

#> 9 Burkin… 75 2.74e5 9242 6 5.17 1.07

#> 10 CAR 94 6.23e5 3127 13 8.08 1.21

#> # … with 64 more rows, and 7 more variables: lang_per_cap <dbl>,

#> # log_lang_per_cap <dbl>, log_area <dbl>, lang_per_cap_std <dbl>,

#> # area_std <dbl>, mean_growing_std <dbl>, sd_growing_std <dbl>We’ll start by fitting two models, one with only mean_growing_std as a predictor, and one that also includes area_std. We can then compare the models using PSIS-LOO.

b8h4a_1 <- brm(lang_per_cap_std ~ mean_growing_std,

data = nettle, family = gaussian,

prior = c(prior(normal(0, 0.2), class = Intercept),

prior(normal(0, 0.5), class = b),

prior(exponential(1), class = sigma)),

iter = 4000, warmup = 2000, chains = 4, cores = 4, seed = 1234,

file = here("fits", "chp8", "b8h4a_1.rds"))

b8h4a_2 <- brm(lang_per_cap_std ~ mean_growing_std + area_std,

data = nettle, family = gaussian,

prior = c(prior(normal(0, 0.2), class = Intercept),

prior(normal(0, 0.5), class = b),

prior(exponential(1), class = sigma)),

iter = 4000, warmup = 2000, chains = 4, cores = 4, seed = 1234,

file = here("fits", "chp8", "b8h4a_2.rds"))

b8h4a_1 <- add_criterion(b8h4a_1, criterion = "loo")

b8h4a_2 <- add_criterion(b8h4a_2, criterion = "loo")

loo_compare(b8h4a_1, b8h4a_2)

#> elpd_diff se_diff

#> b8h4a_1 0.0 0.0

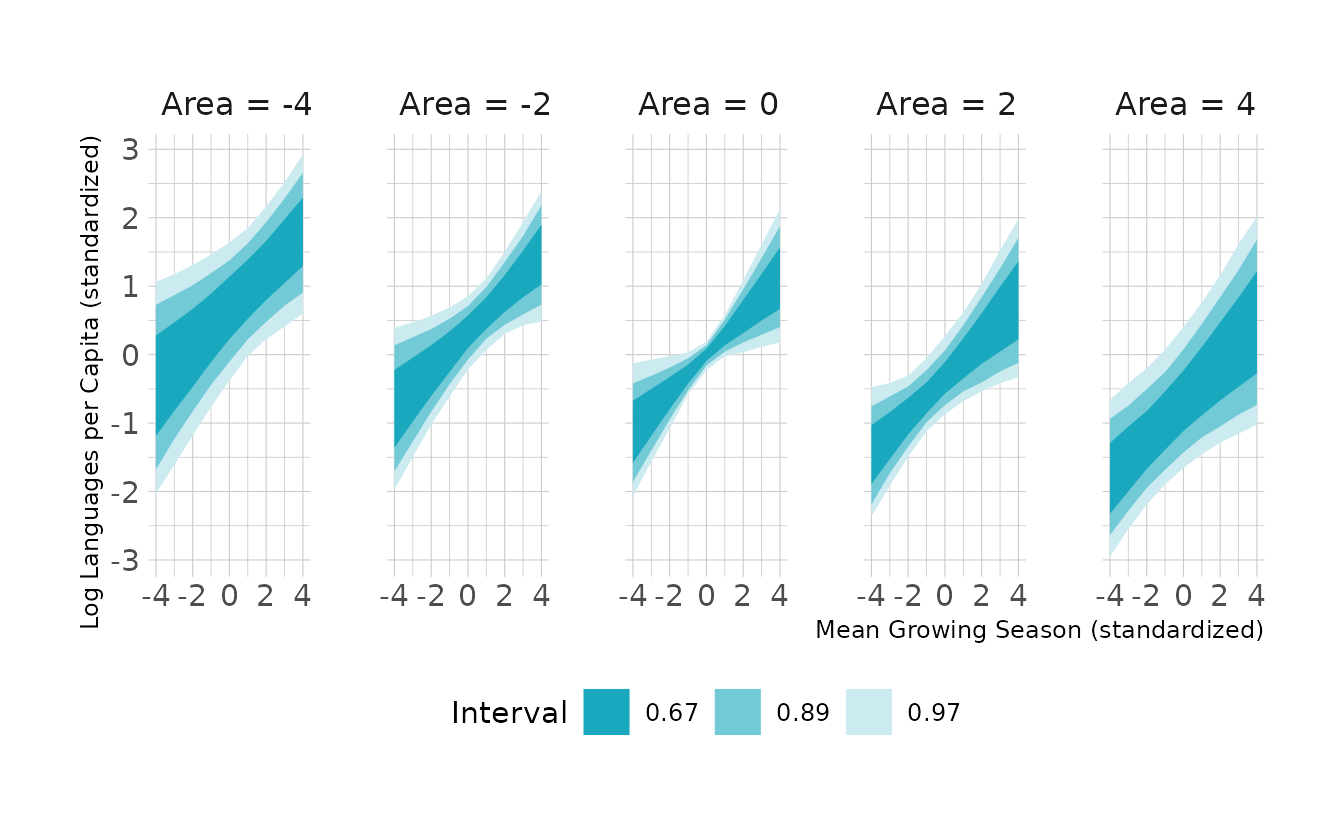

#> b8h4a_2 -0.1 1.6We see that the model without area is slightly preferred, but PSIS-LOO isn’t really able to distinguish between the models very well. For the purpose of this exercise, we’ll continue with model b8h4a_2, which includes both predictors. Visualizing the model, we see that, as expected given the model comparisons, area doesn’t appear to have much impact. However, there does appear to be a positive relationship between the the mean growing season and the number of languages.

new_nettle <- crossing(area_std = seq(-4, 4, by = 2),

mean_growing_std = seq(-4, 4, by = 1),

sd_growing_std = seq(-4, 4, by = 1))

to_string <- as_labeller(c(`-4` = "Area = -4", `-2` = "Area = -2",

`0` = "Area = 0",

`2` = "Area = 2", `4` = "Area = 4"))

new_nettle %>%

add_epred_draws(b8h4a_2, ndraws = 1000) %>%

mean_qi(.width = c(0.67, 0.89, 0.97)) %>%

ggplot(aes(x = mean_growing_std, y = .epred, ymin = .lower, ymax = .upper)) +

facet_wrap(~area_std, nrow = 1, labeller = to_string) +

geom_lineribbon(color = NA) +

scale_fill_manual(values = ramp_blue(seq(0.9, 0.2, length.out = 3)),

breaks = c("0.67", "0.89", "0.97")) +

labs(x = "Mean Growing Season (standardized)",

y = "Log Languages per Capita (standardized)",

fill = "Interval")

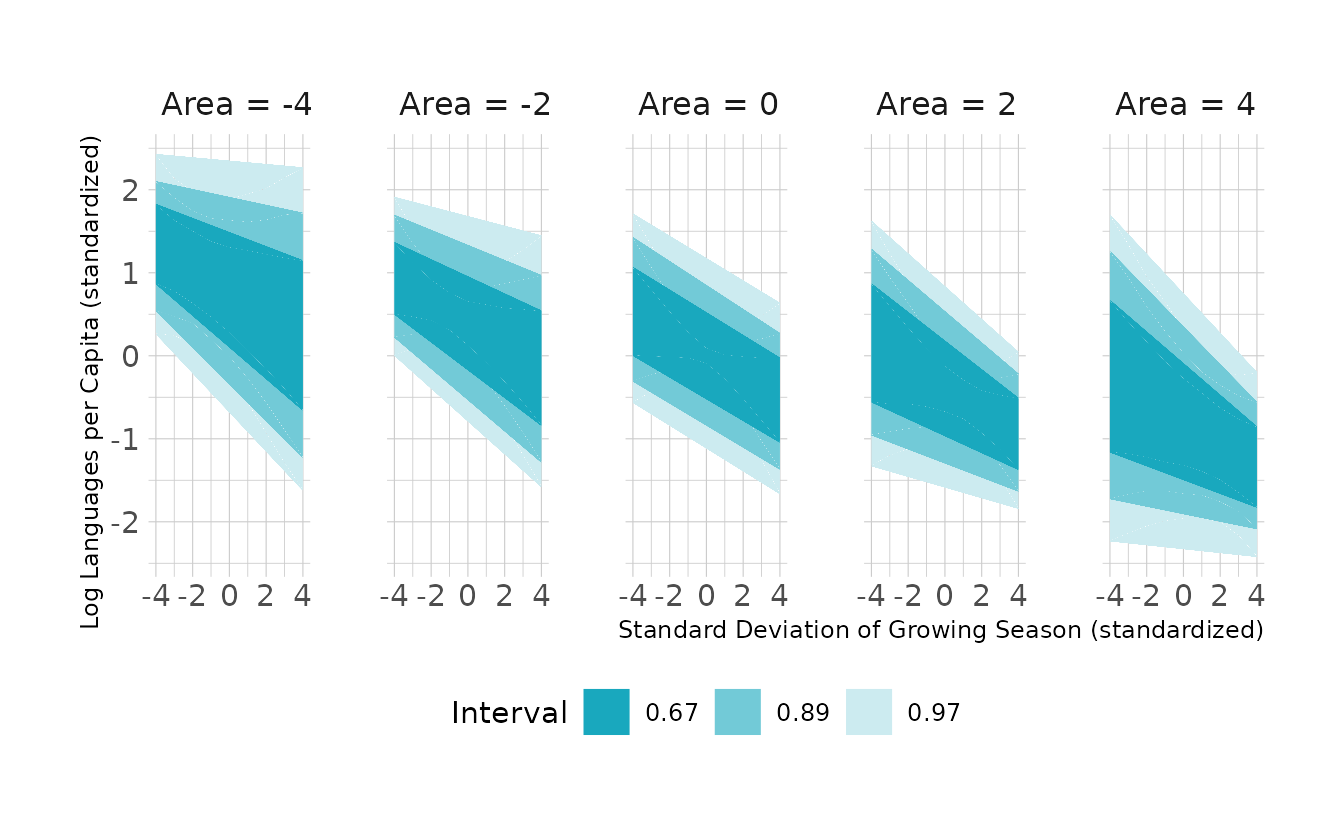

- Now evaluate the hypothesis that language diversity is negatively associated with the standard deviation of length of growing season,

sd.growing.season. This hypothesis follows from uncertainty in harvest favoring social insurance through larger social networks and therefore fewer languages. Again, considerlog(area)as a covariate (not an interaction). Interpret your results.

For the second part, we replace mean_growing_std with sd_growing_std. Again, we’ll fit two models and compare with PSIS-LOO.

b8h4b_1 <- brm(lang_per_cap_std ~ sd_growing_std,

data = nettle, family = gaussian,

prior = c(prior(normal(0, 0.2), class = Intercept),

prior(normal(0, 0.5), class = b),

prior(exponential(1), class = sigma)),

iter = 4000, warmup = 2000, chains = 4, cores = 4, seed = 1234,

file = here("fits", "chp8", "b8h4b_1.rds"))

b8h4b_2 <- brm(lang_per_cap_std ~ sd_growing_std + area_std,

data = nettle, family = gaussian,

prior = c(prior(normal(0, 0.2), class = Intercept),

prior(normal(0, 0.5), class = b),

prior(exponential(1), class = sigma)),

iter = 4000, warmup = 2000, chains = 4, cores = 4, seed = 1234,

file = here("fits", "chp8", "b8h4b_2.rds"))

b8h4b_1 <- add_criterion(b8h4b_1, criterion = "loo")

b8h4b_2 <- add_criterion(b8h4b_2, criterion = "loo")

loo_compare(b8h4b_1, b8h4b_2)

#> elpd_diff se_diff

#> b8h4b_1 0.0 0.0

#> b8h4b_2 0.0 1.7The story here is much the same. PSIS-LOO can’t really differentiate between the two models, indicating that area doesn’t add too much information. This is again reflected in the visualization. We see that the expected distribution of regression lines is fairly similar for all levels of area. Additionally, we do see a negative relationship between the standard deviation of the growing season and the number of languages, as the question suggested.

new_nettle %>%

add_epred_draws(b8h4b_2, ndraws = 1000) %>%

mean_qi(.width = c(0.67, 0.89, 0.97)) %>%

ggplot(aes(x = sd_growing_std, y = .epred, ymin = .lower, ymax = .upper)) +

facet_wrap(~area_std, nrow = 1, labeller = to_string) +

geom_lineribbon(color = NA) +

scale_fill_manual(values = ramp_blue(seq(0.9, 0.2, length.out = 3)),

breaks = c("0.67", "0.89", "0.97")) +

labs(x = "Standard Deviation of Growing Season (standardized)",

y = "Log Languages per Capita (standardized)",

fill = "Interval")

- Finally, evaluate the hypothesis that

mean.growing.seasonandsd.growing.seasoninteract to synergistically reduce language diversity. The idea is that, in nations with longer average growing seasons, high variance makes storage and redistribution even more important than it would be otherwise. That way, people can cooperate to preserve and protect windfalls to be used during the droughts.

In the third part of the question, we are asked to add the interaction term. We’ll drop area since it does not appear to have an effect in either of the previous parts of this question.

b8h4_c <- brm(lang_per_cap_std ~ mean_growing_std * sd_growing_std,

data = nettle, family = gaussian,

prior = c(prior(normal(0, 0.2), class = Intercept),

prior(normal(0, 0.5), class = b),

prior(exponential(1), class = sigma)),

iter = 4000, warmup = 2000, chains = 4, cores = 4, seed = 1234,

file = here("fits", "chp8", "b8h4_c.rds"))

summary(b8h4_c)

#> Family: gaussian

#> Links: mu = identity; sigma = identity

#> Formula: lang_per_cap_std ~ mean_growing_std * sd_growing_std

#> Data: nettle (Number of observations: 74)

#> Draws: 4 chains, each with iter = 2000; warmup = 0; thin = 1;

#> total post-warmup draws = 8000

#>

#> Population-Level Effects:

#> Estimate Est.Error l-95% CI u-95% CI Rhat

#> Intercept 0.00 0.09 -0.18 0.19 1.00

#> mean_growing_std 0.23 0.11 0.01 0.46 1.00

#> sd_growing_std -0.23 0.10 -0.43 -0.03 1.00

#> mean_growing_std:sd_growing_std -0.24 0.11 -0.44 -0.03 1.00

#> Bulk_ESS Tail_ESS

#> Intercept 8427 5784

#> mean_growing_std 7513 6080

#> sd_growing_std 9774 5790

#> mean_growing_std:sd_growing_std 8652 6050

#>

#> Family Specific Parameters:

#> Estimate Est.Error l-95% CI u-95% CI Rhat Bulk_ESS Tail_ESS

#> sigma 0.89 0.08 0.75 1.06 1.00 7972 5945

#>

#> Draws were sampled using sample(hmc). For each parameter, Bulk_ESS

#> and Tail_ESS are effective sample size measures, and Rhat is the potential

#> scale reduction factor on split chains (at convergence, Rhat = 1).We see that the interaction is negative. What this means can be seen by visualizing the interaction from both directions. This is shown in the following image. In the top row, we plot the expected effect of mean growing season on languages. We see that there is a positive relationship between mean growing season and languages, except when there is high variance in the growing. Similarly, the bottom row shows the expected effect of standard deviation of the growing season on languages. When the mean growing season is short, there is no effect of the variance on languages. When the mean growing season is long, there is a negative relationship between variance and languages.

Code to reproduce

library(patchwork)

new_nettle <- crossing(mean_growing_std = seq(-2, 2, by = 0.5),

sd_growing_std = seq(-2, 4, by = 0.5))

int_preds <- new_nettle %>%

add_epred_draws(b8h4_c, ndraws = 1000) %>%

mean_qi(.width = 0.97)

facet_levels <- seq(-2, 2, by = 2)

sd_facets <- list_along(facet_levels)

for (i in seq_along(sd_facets)) {

points <- nettle %>%

mutate(diff = sd_growing_std - facet_levels[i])

p <- int_preds %>%

filter(sd_growing_std == facet_levels[i]) %>%

ggplot(aes(x = mean_growing_std, y = .epred, ymin = .lower,

ymax = .upper)) +

geom_lineribbon(fill = "#99D8E2", color = "black") +

geom_point(data = points,

aes(x = mean_growing_std, y = lang_per_cap_std,

alpha = -1 * abs(diff)), size = 0.5,

inherit.aes = FALSE, show.legend = FALSE) +

expand_limits(x = c(-2, 2), y = c(-2.5, 3.5)) +

labs(x = "Mean growing season", y = "Languages",

subtitle = glue("SD growing season = {facet_levels[i]}")) +

theme(plot.subtitle = element_text(size = 10))

if (i == 2) {

p <- p +

theme(plot.margin = margin(0, 20, 0, 20))

} else {

p <- p +

theme(plot.margin = margin(0, 0, 0, 0))

}

sd_facets[[i]] <- p

}

mean_facets <- list_along(facet_levels)

for (i in seq_along(mean_facets)) {

points <- nettle %>%

mutate(diff = mean_growing_std - facet_levels[i])

p <- int_preds %>%

filter(mean_growing_std == facet_levels[i]) %>%

ggplot(aes(x = sd_growing_std, y = .epred, ymin = .lower,

ymax = .upper)) +

geom_lineribbon(fill = "#99D8E2", color = "black") +

geom_point(data = points,

aes(x = sd_growing_std, y = lang_per_cap_std,

alpha = -1 * abs(diff)), size = 0.5,

inherit.aes = FALSE, show.legend = FALSE) +

expand_limits(x = c(-2, 2), y = c(-2.5, 3.5)) +

labs(x = "SD growing season", y = "Languages",

subtitle = glue("Mean growing season = {facet_levels[i]}")) +

theme(plot.subtitle = element_text(size = 10))

if (i == 2) {

p <- p +

theme(plot.margin = margin(30, 20, 0, 20))

} else {

p <- p +

theme(plot.margin = margin(30, 0, 0, 0))

}

mean_facets[[i]] <- p

}

sd_patch <- (sd_facets[[1]] | sd_facets[[2]] | sd_facets[[3]])

mean_patch <- (mean_facets[[1]] | mean_facets[[2]] | mean_facets[[3]])

sd_patch / mean_patch

8H5. Consider the

data(Wines2012)data table. These data are expert ratings of 20 different French and American wines by 9 different French and American judges. Your goal is to modelscore, the subjective rating assigned by each judge to each wine. I recommend standardizing it. In this problem, consider only variation among judges and wines. Construct index variables ofjudgeandwineand then use these index variables to construct a linear regression model. Justify your priors. You should end up with 9 judge parameters and 20 wine parameters. How do you interpret the variation among individual judges and individual wines? Do you notice any patterns, just by plotting the differences? Which judges gave the highest/lowest ratings? Which wines were rated worst/best on average?

First, let’s prepare the data. We’ll standardize the score and create index variables for both judge and wine.

data(Wines2012)

wine <- Wines2012 %>%

as_tibble() %>%

mutate(score_std = standardize(score),

judge_ind = factor(as.integer(judge)),

wine_ind = factor(as.integer(wine)),

red = factor(flight, levels = c("white", "red")),

wine_amer = factor(wine.amer),

judge_amer = factor(judge.amer))Next, we’ll fit the model, remembering to remove the overall intercept (i.e., ~ 0) so that the index variables are estimated correctly. Because the scores have been standardized, we can use the normal(0, 0.5) prior we’ve used previously and which is used throughout much of the text. We’ll also extract the posterior draws so that we can explore the posterior for each judge and wine individually.

b8h5 <- brm(bf(score_std ~ 0 + j + w,

j ~ 0 + judge_ind,

w ~ 0 + wine_ind,

nl = TRUE),

data = wine, family = gaussian,

prior = c(prior(normal(0, 0.5), nlpar = j),

prior(normal(0, 0.5), nlpar = w),

prior(exponential(1), class = sigma)),

iter = 4000, warmup = 2000, chains = 4, cores = 4, seed = 1234,

file = here("fits", "chp8", "b8h5.rds"))

draws <- as_draws_df(b8h5) %>%

as_tibble() %>%

select(-sigma, -lp__) %>%

pivot_longer(-c(.chain, .iteration, .draw), names_to = c(NA, NA, "type", "num"), names_sep = "_",

values_to = "value", ) %>%

mutate(num = str_replace_all(num, "ind", ""),

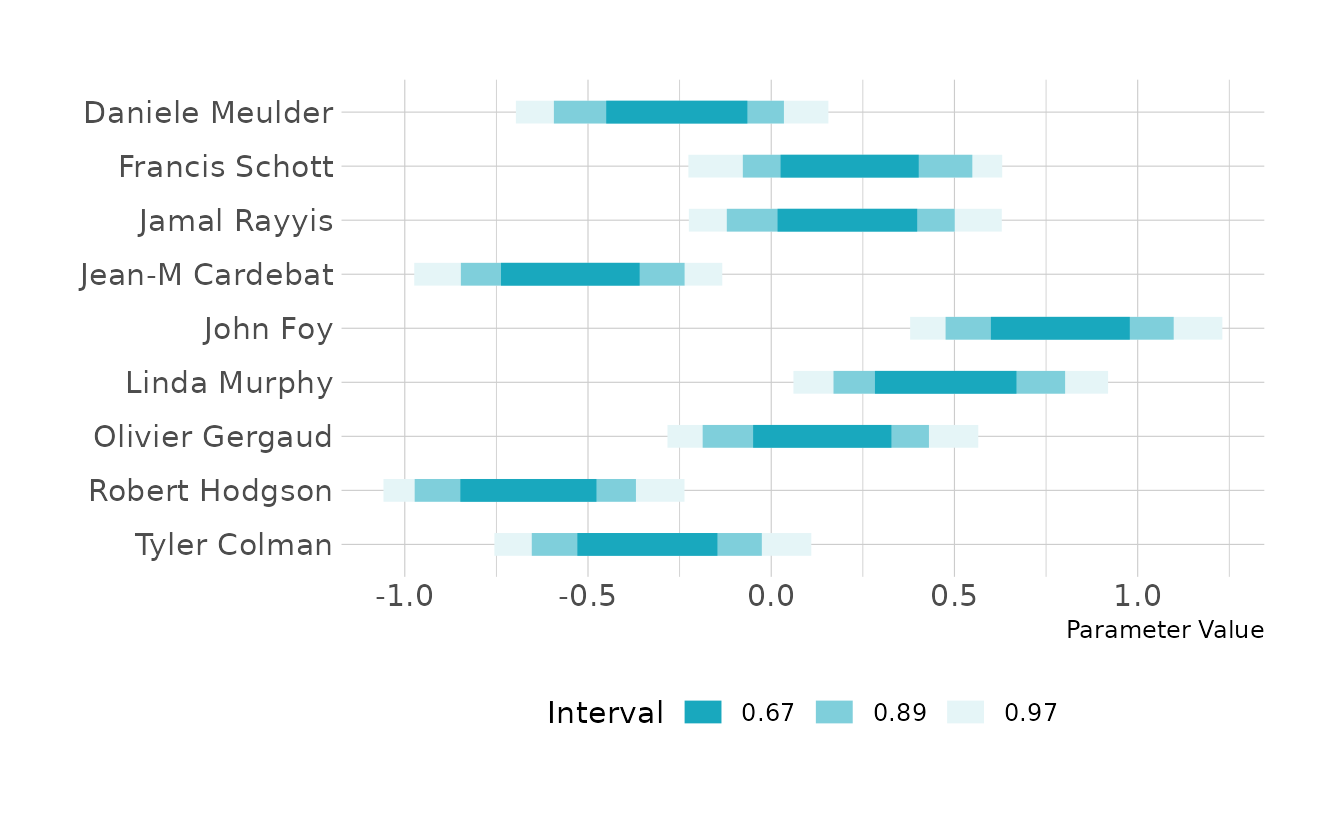

num = as.integer(num))Looking at the distributions by judge, we can see that John Foy tends to give the highest scores, whereas Robert Hodgson and Jean-M Cardebat give the lowest scores on average.

draws %>%

filter(type == "judge") %>%

mutate(num = factor(num)) %>%

left_join(wine %>%

distinct(judge, judge_ind),

by = c("num" = "judge_ind")) %>%

select(judge, value) %>%

group_by(judge) %>%

median_hdci(.width = c(0.67, 0.89, 0.97)) %>%

ggplot(aes(y = fct_rev(judge), x = value, xmin = .lower, xmax = .upper)) +

geom_interval() +

scale_color_manual(values = ramp_blue(seq(0.9, 0.1, length.out = 3)),

limits = as.character(c(0.67, 0.89, 0.97))) +

labs(y = NULL, x = "Parameter Value", color = "Interval")

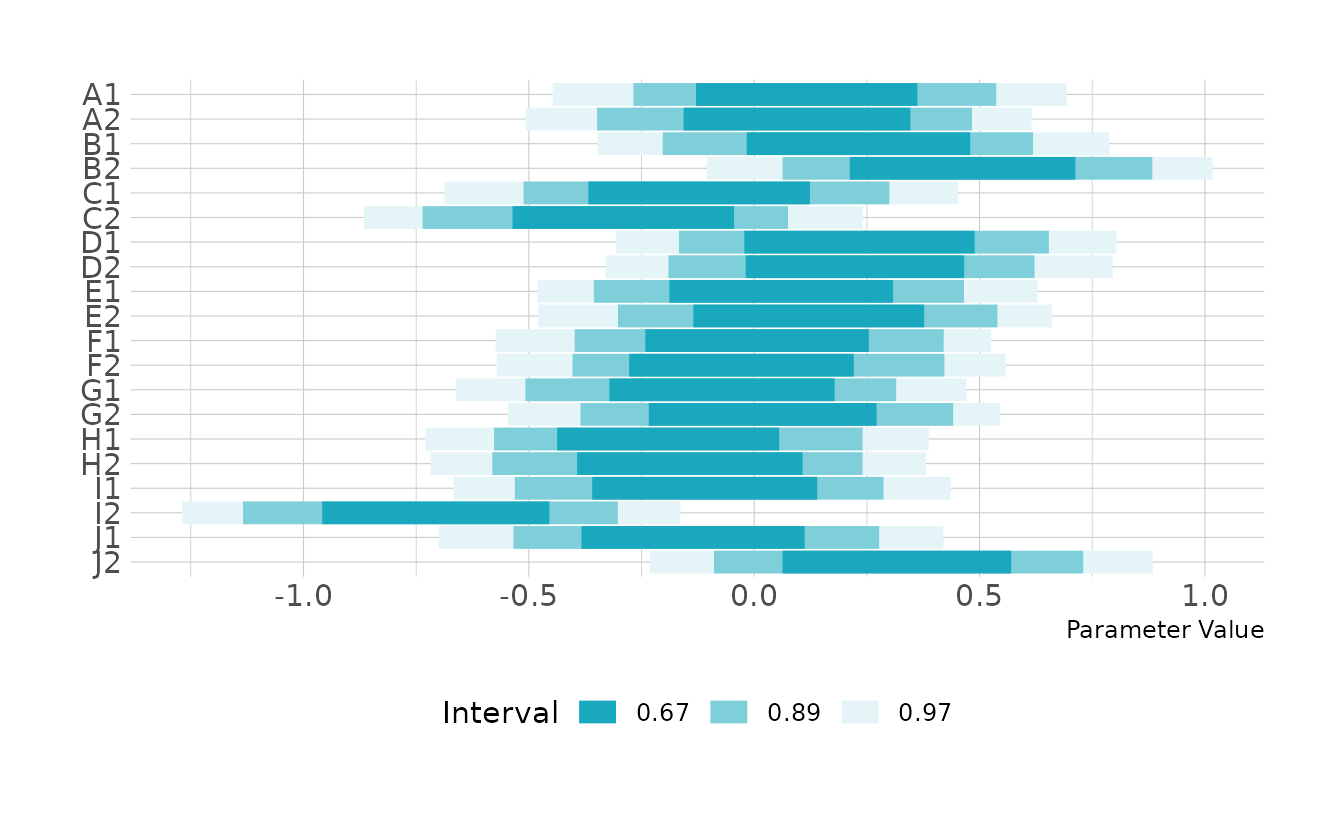

For wines, B2, J2, D2, D1, and B1 received the highest scores on average, and wine I2 was clearly the lowest rated of the wines. However, overall, there is more variability among the judges than among the wines.

draws %>%

filter(type == "wine") %>%

mutate(num = factor(num)) %>%

left_join(wine %>%

distinct(wine, wine_ind),

by = c("num" = "wine_ind")) %>%

select(wine, value) %>%

group_by(wine) %>%

median_hdci(.width = c(0.67, 0.89, 0.97)) %>%

ggplot(aes(y = fct_rev(wine), x = value, xmin = .lower, xmax = .upper)) +

geom_interval() +

scale_color_manual(values = ramp_blue(seq(0.9, 0.1, length.out = 3)),

limits = as.character(c(0.67, 0.89, 0.97))) +

labs(y = NULL, x = "Parameter Value", color = "Interval")

8H6. Now consider three features of the wines and judges:

flight: Whether the wine is red or white.wine.amer: Indicator variable for American wines.judge.amer: Indicator variable for American judges.

Use indicator or index variables to model the influence of these features on the scores. Omit the individual judge and wine index variables from Problem 1. Do not include interaction effects yet. Again justify your priors What do you conclude about the differences among the wines and judges? Try to relate the results to the inferences in the previous problem.

We can estimate the {brms} model as defined below. In this definition, we’re using indicator variables rather than index variables, as that will make the next question a little bit easier. We’ll use our standard normal(0, 0.2) prior for the intercept, since that will have to be near zero given that the score has been standardized. For the coefficients, we have to ask what a reasonable difference in scores would be between New Jersey and French wines, New Jersey and French judges, and red and white wine. One standard deviation seems to be the edge of what might be reasonable, so we’ll use normal(0, 0.5), as that will leave sufficient probability in the tails. These priors constrain the space to plausible values, but we could probably use tighter priors on the slope parameters if we wanted to get more regularization.

b8h6 <- brm(score_std ~ wine_amer + judge_amer + red,

data = wine, family = gaussian,

prior = c(prior(normal(0, 0.2), class = Intercept),

prior(normal(0, 0.5), class = b),

prior(exponential(1), class = sigma)),

iter = 4000, warmup = 2000, chains = 4, cores = 4, seed = 1234,

file = here("fits", "chp8", "b8h6.rds"))

fixef(b8h6)

#> Estimate Est.Error Q2.5 Q97.5

#> Intercept -0.01641 0.157 -0.3237 0.287

#> wine_amer1 -0.17688 0.145 -0.4640 0.109

#> judge_amer1 0.22773 0.143 -0.0534 0.503

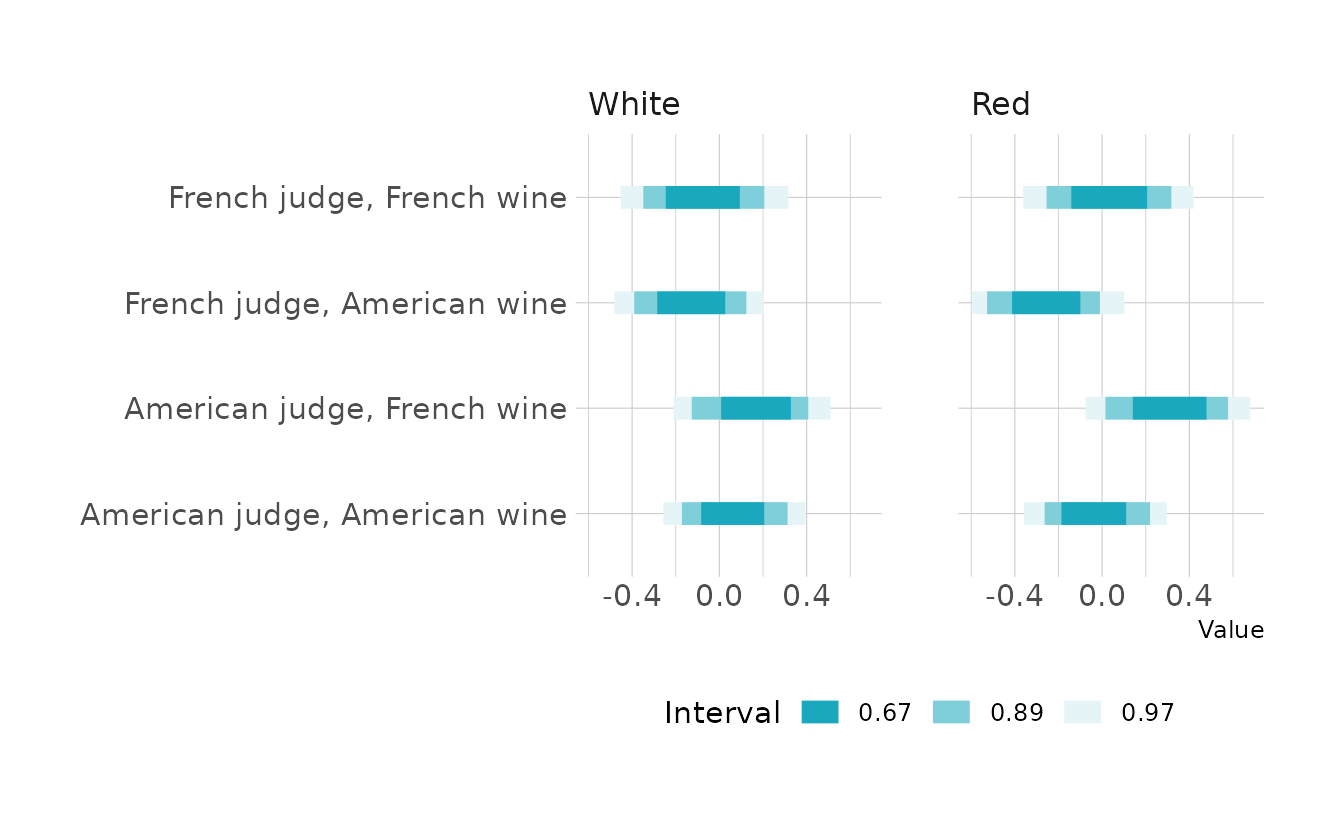

#> redred -0.00686 0.145 -0.2873 0.277As indicated by the last problem, there is basically no effect of red vs. white wine. There does appear to be a slight preference for French wines; however, there’s a good deal of posterior density on both sides of 0. This confirms what we found in the last problem: that there is little variation coming from the wines. We do see a slightly stronger effect among judges, with American judges giving higher scores on average.

8H7. Now consider two-way interactions among the three features. You should end up with three different interaction terms in your model. These will be easier to build, if you use indicator variables. Again justify your priors. Explain what each interaction means. Be sure to interpret the model’s predictions on the outcome scale (

mu, the expected score), not on the scale of individual parameters. You can uselinkto help with this, or just use your knowledge of the linear model instead. What do you conclude about the features and the scores? Can you relate the results of your model(s) to the individual judge and wine inferences from 8H5?

We’ll start by fitting the model. Here I’ve used the same priors as the previous problem for the intercept and main effect parameters. For the interactions, I have specified a normal(0, 0.25) prior. The interaction priors are a little tighter because as we keep subsetting the sample, values can’t keep getting larger and larger.

b8h7 <- brm(score_std ~ wine_amer + judge_amer + red +

wine_amer:judge_amer + wine_amer:red + judge_amer:red,

data = wine, family = gaussian,

prior = c(prior(normal(0, 0.2), class = Intercept),

prior(normal(0, 0.5), class = b),

prior(normal(0, 0.25), class = b,

coef = judge_amer1:redred),

prior(normal(0, 0.25), class = b,

coef = wine_amer1:judge_amer1),

prior(normal(0, 0.25), class = b,

coef = wine_amer1:redred),

prior(exponential(1), class = sigma)),

iter = 4000, warmup = 2000, chains = 4, cores = 4, seed = 1234,

file = here("fits", "chp8", "b8h7.rds"))

fixef(b8h7)

#> Estimate Est.Error Q2.5 Q97.5

#> Intercept -0.0749 0.176 -0.420 0.274

#> wine_amer1 -0.0553 0.193 -0.419 0.324

#> judge_amer1 0.2258 0.194 -0.158 0.603

#> redred 0.1028 0.198 -0.280 0.494

#> wine_amer1:judge_amer1 -0.0314 0.186 -0.396 0.325

#> wine_amer1:redred -0.2335 0.188 -0.596 0.136